Many people search for a bankruptcies lawyer when the bills, collection calls, court papers, or mortgage arrears become too much to manage alone. The better term is bankruptcy lawyer, but the concern behind the search is clear: you need to know whether the law can give you breathing room, and you need to choose someone you can trust.

Bankruptcy is not right for everyone. It is also not a personal failure. For many New York consumers, homeowners, and small business owners, bankruptcy can be a practical legal tool for stopping creditor pressure, reorganizing debt, protecting wages, and, in some cases, creating a path to keep a home.

Before hiring an attorney, it helps to understand what a good bankruptcy consultation should cover, what questions to ask, and what warning signs to avoid.

Bankruptcy is a legal tool, not a last-resort label

The U.S. Courts describe bankruptcy as a legal process that helps people and businesses who cannot repay debts. That process can be powerful, but it must be used carefully.

One of the most important protections is the automatic stay. In many cases, once a bankruptcy petition is filed, the automatic stay temporarily stops collection activity. Depending on the circumstances, this may pause wage garnishments, creditor lawsuits, collection calls, bank restraints, repossessions, and foreclosure activity.

That does not mean bankruptcy erases every problem or guarantees that a home, car, or business will be saved. A good bankruptcy lawyer should explain both the benefits and the limits. The goal is not simply to file a case. The goal is to choose the right strategy for your financial reality.

When should you speak with a bankruptcy lawyer?

Many people wait until the situation feels unbearable. Unfortunately, waiting can reduce available options, especially if a foreclosure sale, wage garnishment, eviction, or creditor judgment is already moving forward.

You should consider speaking with a bankruptcy lawyer if:

- You are behind on mortgage payments and have received foreclosure papers.

- You have a scheduled foreclosure auction or fear one may be coming.

- You are being sued by a credit card company, debt buyer, lender, or medical creditor.

- Your wages are being garnished or your bank account has been restrained.

- You cannot keep up with credit cards, personal loans, medical bills, or tax obligations.

- You are a landlord, small business owner, or self-employed person facing business-related debt.

- You are considering a debt settlement program but are unsure whether it is safe or realistic.

Bankruptcy is often most effective when it is evaluated before deadlines pass. Even if you ultimately decide not to file, a consultation can help you understand your legal position.

Understand which type of bankruptcy may apply

Not all bankruptcies work the same way. The chapter that fits one person may be completely wrong for another. A responsible attorney should explain the differences in plain language and connect the recommendation to your goals.

| Bankruptcy chapter | Common purpose | Why it may matter |

| Chapter 7 | Liquidation bankruptcy for qualifying individuals or businesses | May eliminate many unsecured debts, such as credit cards and medical bills, but asset protection must be carefully reviewed. |

| Chapter 13 | Repayment plan for individuals with regular income | May help homeowners catch up on mortgage arrears over time while maintaining ongoing payments. |

| Chapter 11 | Reorganization for businesses and certain individuals with complex debts | May allow a business to restructure debt while continuing operations, depending on the facts. |

For many consumers, the choice is between Chapter 7 and Chapter 13. Chapter 7 may be appropriate for someone with limited income and mostly unsecured debt. Chapter 13 may be more useful for a homeowner who has fallen behind on mortgage payments but has enough income to make ongoing payments and a court-approved plan payment.

If you are unsure where you fit, you may find it helpful to review CGW’s guide on Chapter 7 vs. Chapter 13 bankruptcy in Westchester and the Hudson Valley. Still, your own situation should be reviewed by an attorney before you make decisions.

Why New York bankruptcy experience matters

Bankruptcy is federal law, but local practice still matters. For many residents of Westchester, Rockland, Putnam, Orange, Dutchess, and Bronx Counties, bankruptcy cases are handled in the U.S. Bankruptcy Court for the Southern District of New York, including the White Plains division depending on venue.

A lawyer familiar with New York practice should understand local procedures, trustee expectations, foreclosure timing, state court litigation, and the interaction between bankruptcy and New York property rights. This can be especially important for homeowners.

New York residents must also carefully evaluate exemptions. Exemptions are laws that may protect certain property in bankruptcy, such as equity in a home, a vehicle, retirement funds, household goods, or other assets. In New York, debtors may often need to compare New York exemptions and federal exemptions, but they generally cannot mix and match between systems. The better choice depends on the property you own, the equity you have, and your overall goals.

This is one reason a quick form-based filing or one-size-fits-all approach can be risky. Small details can have major consequences.

What a bankruptcy lawyer should review before recommending a filing

A bankruptcy lawyer should not recommend filing based only on your total debt. The attorney should look at your full financial picture, including your income, assets, household expenses, secured debts, lawsuits, tax history, and property transfers.

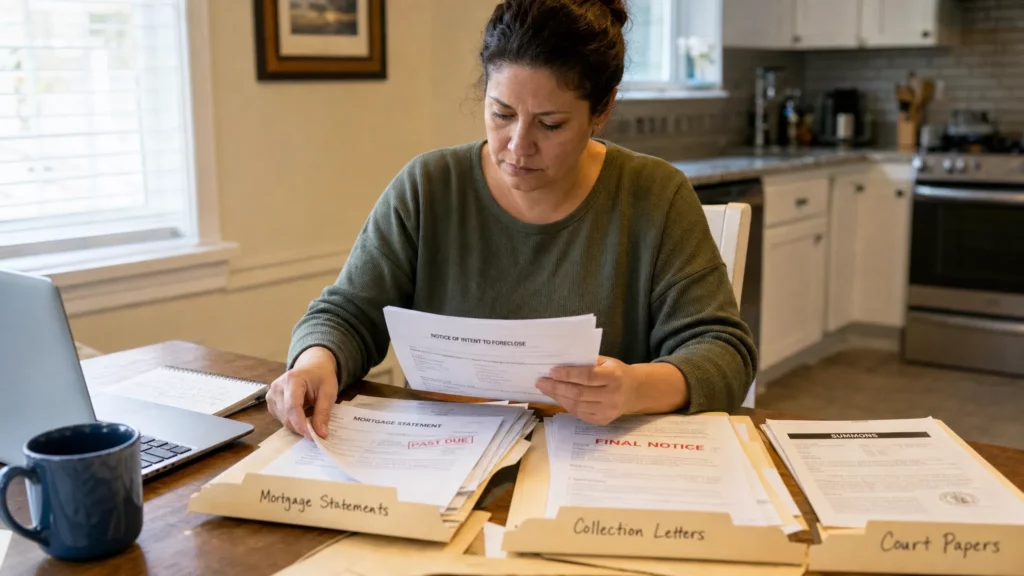

Before or during your consultation, try to gather:

- Recent pay stubs, profit and loss information, or other income records.

- Mortgage statements, foreclosure notices, and court papers.

- Credit card bills, medical bills, personal loan statements, and collection letters.

- Tax returns, tax notices, and information about any unpaid taxes.

- Bank statements and retirement account statements.

- Vehicle loan statements, leases, and title information.

- Any lawsuits, judgments, wage garnishment notices, or bank restraint documents.

The lawyer should ask about recent payments to relatives, property transfers, refinancing, business interests, prior bankruptcies, and expected changes in income. These questions are not meant to judge you. They help the attorney spot risks before they become problems.

Questions to ask before hiring a bankruptcy lawyer

The right lawyer should welcome practical questions. You are not just hiring someone to prepare forms. You are hiring someone to help you evaluate risk, timing, and strategy during a stressful financial period.

| Question to ask | Why it matters |

| Have you handled cases like mine? | A homeowner facing foreclosure has different concerns than someone with only credit card debt. |

| Which chapter do you believe may fit my situation, and why? | The answer should be tied to your income, assets, debts, and goals. |

| What are the risks of filing? | Every bankruptcy case has potential downsides, including asset, credit, timing, or eligibility issues. |

| How will bankruptcy affect my home, car, wages, or business? | Secured property and income issues need careful review before filing. |

| Are there non-bankruptcy options I should consider? | Bankruptcy may be one option among foreclosure defense, loan modification, settlement, or debt defense. |

| What fees and costs should I expect? | You should understand attorney fees, court filing fees, required courses, and what services are included. |

| Who will handle my case day to day? | Clear communication matters, especially when deadlines are involved. |

| What deadlines should I be worried about right now? | Foreclosure sales, answer deadlines, garnishments, and court dates may require immediate action. |

A clear attorney-client relationship should include a written retainer agreement that explains the scope of representation. If you do not understand what is included, ask before signing.

Warning signs to watch for

Most bankruptcy lawyers are serious professionals, but consumers in financial distress can be vulnerable to poor advice. Be cautious if someone treats bankruptcy like a quick transaction without reviewing your documents or goals.

Warning signs may include:

- Promises that all debts will definitely disappear.

- Guarantees that you will keep your home or stop foreclosure permanently.

- Pressure to sign immediately without time to ask questions.

- Vague or changing fee explanations.

- Advice to hide assets, transfer property, or leave information out of court documents.

- A refusal to discuss alternatives or risks.

- A non-lawyer company offering legal advice about foreclosure, debt, or bankruptcy.

Bankruptcy petitions are signed under penalty of perjury. Accuracy matters. A lawyer should help you disclose information properly, not avoid disclosure.

Fees are important, but cheapest is not always safest

Cost matters when you are already under financial pressure. You should absolutely ask about fees, payment arrangements, court costs, and what services are included. At the same time, the lowest advertised fee may not be the best value if the lawyer does not review your home equity, foreclosure status, tax issues, prior filings, business interests, or lawsuit deadlines.

A poorly planned bankruptcy can lead to dismissal, loss of protection, unnecessary litigation, or avoidable stress. In a Chapter 13 case, an unrealistic plan can fail if the monthly payment does not match your actual budget. In a Chapter 7 case, failing to analyze assets and exemptions can create serious problems.

The right question is not only, how much does it cost? It is also, what legal analysis am I receiving for that cost?

If you own a home, bankruptcy and foreclosure strategy must be coordinated

For New York homeowners, bankruptcy may overlap with foreclosure defense, loan modification, loss mitigation, short sale planning, or post-judgment strategy. Filing bankruptcy without coordinating it with the foreclosure case can cause confusion or missed opportunities.

For example, Chapter 13 may help some homeowners spread mortgage arrears over a repayment plan while they resume regular mortgage payments. In other situations, bankruptcy may provide temporary breathing room while the homeowner evaluates a loan modification, sale, settlement, or other option. Chapter 7 may stop collection activity for a time, but it usually does not create a long-term mortgage arrears repayment plan.

Timing is especially important if a foreclosure auction has already been scheduled. The automatic stay can be powerful, but prior bankruptcy cases, repeat filings, motions for relief from stay, or post-sale issues can affect what protection is available. Every case is unique.

CGW has written more about this issue in When Foreclosure and Bankruptcy Overlap for New York Homeowners and How Chapter 13 Bankruptcy Can Help Stop Foreclosure in NY. If you are facing foreclosure, do not assume it is too early or too late to ask for help. Options may still exist, but they often depend on timing.

What to do before your first consultation

You do not need to have everything perfectly organized before contacting a lawyer. Still, a little preparation can make the consultation more productive.

Before you meet with an attorney:

- Open and save all court papers, foreclosure notices, collection letters, and lender mail.

- Write down key dates, including court appearances, sale dates, default notices, and garnishment dates.

- Make a rough list of debts, assets, income, and monthly expenses.

- Avoid transferring property, repaying relatives, or draining retirement accounts without legal advice.

- Be honest about prior bankruptcies, lawsuits, tax debt, and property ownership.

If there is an urgent deadline, tell the attorney immediately when you call. A foreclosure auction, eviction date, wage garnishment, or lawsuit answer deadline can change the priority of the legal strategy.

What happens after you hire a bankruptcy lawyer?

After you hire a lawyer, the next steps depend on the type of case and your goals. Typically, the attorney will collect documents, analyze eligibility, review exemptions, identify risks, and advise whether bankruptcy or another option makes sense.

If bankruptcy is appropriate, you may need to complete required credit counseling before filing. Your lawyer will prepare the bankruptcy petition, schedules, statements, and related documents. These papers disclose your debts, assets, income, expenses, transfers, and financial history.

Once the case is filed, the automatic stay generally goes into effect, subject to important exceptions. You will also attend a meeting of creditors, often called a 341 meeting, where a trustee asks questions about your filing. In Chapter 13, you must also propose and maintain a repayment plan. In Chapter 7, the case may move toward discharge if there are no objections or complications.

A good lawyer should keep you informed about what to expect, what you must provide, and what deadlines matter.

Frequently Asked Questions

Do I really need a lawyer to file bankruptcy? Individuals can file without an attorney, but bankruptcy is document-heavy and mistakes can be costly. If you own a home, face foreclosure, have significant assets, owe taxes, operate a business, or have been sued, legal guidance is especially important.

Can a bankruptcy lawyer stop foreclosure immediately? Filing bankruptcy may trigger the automatic stay, which can temporarily stop many foreclosure actions. However, timing, prior filings, court orders, and lender motions can affect the result. Speak with a lawyer as early as possible if a sale date is pending.

Will I lose my home if I file bankruptcy? Not necessarily. Whether you can keep your home depends on the chapter filed, your equity, exemptions, mortgage arrears, income, and ability to maintain payments. Homeowners should get a careful exemption and foreclosure analysis before filing.

Will bankruptcy erase all of my debts? Some debts may be dischargeable, but others may survive bankruptcy. Domestic support obligations, certain taxes, criminal fines, some student loans, and debts involving fraud or misconduct may require special analysis.

Should I try debt settlement before calling a bankruptcy lawyer? Debt settlement may help some people, but it can also create tax issues, collection lawsuits, and delays. A bankruptcy lawyer can compare settlement, debt defense, loan modification, and bankruptcy so you can make a more informed decision.

How soon should I contact a lawyer if I received foreclosure papers? As soon as possible. New York foreclosure cases involve deadlines, settlement conferences, possible defenses, and court procedures. Waiting can limit the strategies available to protect your home.

Talk with a New York bankruptcy lawyer before options narrow

If you are overwhelmed by debt, facing foreclosure, or worried about a creditor lawsuit, you do not have to figure it out alone. The most important step is getting reliable information before deadlines pass.

Clair Gjertsen & Weathers PLLC helps individuals, homeowners, consumers, landlords, tenants, and small businesses throughout Westchester County, Rockland County, Putnam County, Orange County, Dutchess County, Bronx County, and the Lower Hudson Valley evaluate bankruptcy, foreclosure defense, loan modification, and debt relief options.

Every case is different. A conversation with experienced counsel can help you understand what may be available in your situation and what steps should be taken next. If you are considering bankruptcy or have already been served with legal papers, contact Clair Gjertsen & Weathers PLLC to discuss your options before critical deadlines pass.