NY & CT Foreclosure & Bankruptcy Attorneys

Schedule A Free Consultation 914.472.6202

When debt starts to affect your home, paycheck, bank account, or peace of mind, the number of possible solutions can feel overwhelming. You may hear about debt settlement, creditor negotiations, debt consolidation, foreclosure defense, and bankruptcy, often from people who are not looking at your full legal and financial picture.

A debt resolution attorney can help you sort through those choices. In some cases, attorney-led negotiation or debt lawsuit defense may be enough. In others, bankruptcy may provide stronger and faster protection, especially if you are facing lawsuits, wage garnishment, foreclosure, or debts you realistically cannot repay.

The right answer depends on your income, assets, home equity, lawsuit deadlines, creditor pressure, and long-term goals. For New York homeowners and consumers, the most important step is to compare your options before a judgment, foreclosure sale, or missed court deadline limits what can be done.

Start With the Real Problem You Need to Solve

“Debt resolution” can mean different things depending on the situation. For one person, it may mean negotiating credit card balances. For another, it may mean defending a collection lawsuit, stopping a bank restraint, or finding a way to keep a home after falling behind on the mortgage.

Before deciding between a debt resolution attorney and bankruptcy, ask what problem is most urgent:

- Are you being sued by a creditor?

- Has your bank account been restrained?

- Are your wages being garnished?

- Are you behind on your mortgage?

- Have you received foreclosure papers?

- Do you have one major debt or several debts with multiple creditors?

- Do you have enough income to make reduced payments?

- Are you trying to protect a home, car, business, or other property?

New York consumers should be especially careful about ignoring legal papers. A creditor lawsuit can lead to a judgment, and a judgment can create serious collection risks. If you own a home, debt problems can also affect your property. CGW has discussed how debt lawsuits can threaten a homeowner’s income and property, which is one reason early legal advice matters.

What a Debt Resolution Attorney May Do Outside Bankruptcy

A debt resolution attorney focuses on solving debt problems through legal analysis, negotiation, defense, and strategy. Bankruptcy may be one possible tool, but it is not the only one.

Outside bankruptcy, an attorney may help by reviewing whether the creditor can prove the debt, responding to a summons, negotiating a settlement, arranging payment terms, challenging improper collection activity, or protecting exempt income and assets. If the debt is tied to a mortgage or foreclosure, the attorney may also evaluate loan modification options, loss mitigation, foreclosure defenses, or alternatives such as a short sale.

This is different from working with a non-lawyer debt settlement company. A debt settlement company may focus primarily on negotiating balances. A lawyer can also evaluate lawsuits, court deadlines, judgment risks, bankruptcy consequences, lien issues, home equity, and defenses under New York and federal law.

Debt resolution may be a strong fit when the debt is limited, the creditor’s proof is weak, the consumer has funds available for a settlement, or the goal is to resolve a lawsuit without filing bankruptcy. It may also fit when a homeowner is not overwhelmed by all debts but needs focused help with a particular creditor, mortgage servicer, or collection case.

That said, negotiation has limits. A creditor does not have to accept a settlement. Interest and fees may continue. A lawsuit may still move forward unless properly defended. A settlement may also create tax consequences depending on the circumstances. These are reasons to get advice before assuming a negotiated deal is safer or less expensive than bankruptcy.

What Bankruptcy Can Do That Negotiation Usually Cannot

Bankruptcy is not a personal failure. It is a legal process designed to give individuals, families, and businesses a structured way to address debt. In many cases, it can provide protections that private negotiation cannot.

One of the most important protections is the automatic stay. When a bankruptcy case is filed, the automatic stay generally pauses most collection activity, including many lawsuits, wage garnishments, bank restraints, collection calls, and foreclosure activity. There are exceptions, and timing matters, but the automatic stay can be powerful when creditors are moving quickly.

The most common consumer bankruptcy chapters are Chapter 7 and Chapter 13. Chapter 7 is often used to eliminate qualifying unsecured debts, such as credit card debt and medical debt, when the person qualifies and has no unacceptable asset risk. Chapter 13 is a repayment plan that can help some homeowners catch up on mortgage arrears over time while keeping current on ongoing payments.

Small businesses or individuals with more complex financial circumstances may need to consider Chapter 11. This can allow for restructuring, but it is more involved and should be evaluated carefully with counsel.

If you are new to the process, CGW’s overview of consumer bankruptcy basics explains the general differences between the available chapters and how bankruptcy can affect debts, property, and creditor collection.

Debt Resolution Attorney vs. Bankruptcy: A Practical Comparison

The best option is not always the option that sounds least serious. Sometimes negotiation is enough. Sometimes waiting too long to file bankruptcy can make the situation harder. The following comparison can help frame the discussion.

| Option | Often fits when | Potential benefits | Important limits |

|---|---|---|---|

| Attorney-led debt resolution | You have one or a few debts, a pending lawsuit, or funds to negotiate | May avoid bankruptcy, can address lawsuit defenses, may reduce balances or create payment terms | Creditors do not have to settle, lawsuits require timely responses, settlements may have tax or credit consequences |

| Chapter 7 bankruptcy | You have mostly unsecured debt and limited ability to repay | May discharge qualifying debts and stop many collection actions | Not all debts are dischargeable, asset and income issues must be reviewed |

| Chapter 13 bankruptcy | You have regular income and need time to catch up, especially on mortgage arrears | May stop foreclosure and allow structured repayment over time | Requires plan payments, ongoing income, and court approval |

| Chapter 11 bankruptcy | You own a business or have complex debt that needs restructuring | May allow continued operations while reorganizing debt | More complex and typically more expensive than consumer chapters |

No chart can replace legal advice. The same debt amount can lead to different recommendations depending on home equity, household income, creditor behavior, and case timing.

When Attorney-Led Debt Resolution May Be the Better First Step

Debt resolution may be worth exploring before bankruptcy when the problem is contained and there is a realistic path to settlement or defense. For example, if one credit card company filed suit but the consumer has defenses, exemptions, or limited funds available for a lump-sum settlement, a negotiated resolution may make sense.

It can also help when the amount in dispute is uncertain. Debt buyers, for example, must prove that they own the debt and that the amount claimed is accurate. If documentation is incomplete or the lawsuit has procedural problems, legal defense may improve the consumer’s position.

For small business owners, debt resolution can also involve protecting the assets needed to keep income coming in. A contractor, retailer, landlord, or service business may need to identify essential tools, inventory, vehicles, equipment, or shipping containers used for business storage before deciding whether settlement, restructuring, or bankruptcy is the better path.

Attorney-led resolution may be especially helpful when you want to avoid a bankruptcy filing and have enough income or resources to support a deal. The key is to be realistic. If the settlement terms are unaffordable, the agreement may only delay the problem.

When Bankruptcy May Fit Better

Bankruptcy may be a better fit when the debt is widespread, creditor pressure is escalating, or private negotiation cannot provide enough protection. If several creditors are suing, wages are being garnished, bank accounts are being restrained, or collection calls are constant, bankruptcy may offer a more complete framework.

For homeowners, bankruptcy may be particularly important when mortgage arrears are part of the problem. Chapter 13 may allow qualifying homeowners to repay missed mortgage payments over time while staying current on future payments. In some cases, bankruptcy can also create a structured setting for loss mitigation or mortgage review.

Chapter 7 may be appropriate when the primary goal is to eliminate qualifying unsecured debt and the consumer does not need a long-term repayment plan. However, homeowners must be careful. Home equity, exemptions, liens, mortgage status, and other assets should be reviewed before filing. A bankruptcy that is helpful for one person may create avoidable risk for another if filed without careful planning.

Bankruptcy may also be preferable if creditor negotiation would take too long. If a foreclosure sale date, garnishment, or judgment enforcement deadline is approaching, the speed and legal force of the automatic stay may matter. The U.S. Courts bankruptcy basics page provides a general overview of the federal bankruptcy system, but New York-specific advice is important before making a decision.

For Homeowners, the Choice Can Affect Foreclosure Strategy

If you are behind on your mortgage, the decision is rarely just “debt settlement or bankruptcy.” You may also need to consider foreclosure defense, loan modification, loss mitigation, settlement conferences, Chapter 13, Chapter 7, short sale options, or an appeal if a court has already ruled against you.

New York foreclosure cases have their own procedures and timelines. Homeowners may have defenses if the lender or servicer failed to follow required rules, lacked proper documentation, misapplied payments, mishandled a modification application, or failed to comply with applicable notice requirements. These issues should be reviewed before assuming foreclosure is inevitable.

Bankruptcy can sometimes help stop foreclosure activity, but it must be used carefully. Filing too early, too late, or under the wrong chapter can affect your options. If foreclosure is part of your debt problem, CGW’s guide to foreclosure and bankruptcy options for New York homeowners may help you understand how the two areas overlap.

How a New York Debt Resolution Attorney Evaluates the Right Fit

A debt resolution attorney should not recommend bankruptcy or settlement in a vacuum. The analysis should begin with a full review of the facts.

Important factors include your monthly income, expenses, household size, home value, mortgage balance, liens, car loans, retirement accounts, pending lawsuits, judgments, creditor names, tax debts, student loans, and business obligations. The attorney should also ask what outcome matters most to you. Keeping a home, stopping garnishment, protecting a small business, and eliminating unsecured debt may require different strategies.

For homeowners in Westchester County, Rockland County, Putnam County, Orange County, Dutchess County, the Bronx, and the Lower Hudson Valley, local court procedures and New York exemption rules can make a significant difference. The right plan should reflect both the law and the practical realities of your household.

A careful legal review may show that negotiation is sensible. It may show that bankruptcy offers the cleanest path forward. It may also show that a combined strategy is best, such as defending a lawsuit while preparing for bankruptcy if negotiations fail, or pursuing a loan modification while evaluating Chapter 13 as a backup option.

Questions to Ask Before You Decide

Before choosing a path, consider asking an attorney these questions:

- What happens if I do nothing for the next 30, 60, or 90 days?

- Are there court deadlines I cannot miss?

- Can the creditor prove the debt and the amount claimed?

- Do I have income or assets that creditors can reach?

- Would settlement actually be affordable?

- Would bankruptcy protect my home, car, wages, or bank account?

- Which debts would likely survive bankruptcy?

- Could Chapter 13 help with mortgage arrears?

- Are there foreclosure defenses or loan modification options?

- What are the risks of each option in my specific situation?

The goal is not to choose the option with the best marketing. The goal is to choose the option that protects your legal rights and gives you the most realistic path forward.

Frequently Asked Questions

Is a debt resolution attorney the same as a bankruptcy attorney? Not always. A debt resolution attorney may negotiate with creditors, defend debt lawsuits, evaluate foreclosure issues, and advise on bankruptcy. Some attorneys handle both debt resolution and bankruptcy, which can be helpful because they can compare all available options rather than pushing only one strategy.

Is debt settlement better than bankruptcy? It depends. Debt settlement may work if you have a manageable number of debts and money available to fund a reasonable agreement. Bankruptcy may be better if you have multiple creditors, lawsuits, garnishments, foreclosure pressure, or no realistic ability to settle.

Can bankruptcy stop a debt lawsuit in New York? Bankruptcy generally stops many debt lawsuits through the automatic stay, but there are exceptions. If you have already been sued, you should speak with an attorney quickly because lawsuit deadlines may still matter if bankruptcy is not filed or if the stay does not apply to a particular issue.

Can I keep my house if I file bankruptcy? Many homeowners can keep their homes in bankruptcy, depending on income, equity, exemptions, mortgage status, and the chapter filed. Chapter 13 may help some homeowners catch up on mortgage arrears, while Chapter 7 requires careful review of equity and exemptions before filing.

Should I wait until creditors get more aggressive before calling a lawyer? Waiting often reduces options. A debt problem is usually easier to address before a default judgment, wage garnishment, bank restraint, foreclosure sale, or eviction deadline. Early advice does not mean you must file bankruptcy, but it can help you avoid preventable mistakes.

Speak With CGW Before Deadlines Limit Your Options

If you are deciding between a debt resolution attorney and bankruptcy, you do not have to make that decision alone. The right choice depends on your debts, assets, income, court deadlines, and goals for your home or business.

Clair Gjertsen & Weathers PLLC helps New York homeowners, consumers, landlords, tenants, and small businesses evaluate practical solutions for debt, foreclosure, bankruptcy, and related legal problems. If you are facing creditor lawsuits, mortgage default, collection pressure, or uncertainty about bankruptcy, speaking with experienced counsel early may give you more options.

Contact CGW to discuss your situation and begin identifying a path that fits your circumstances. Every case is unique, and timely guidance can make a meaningful difference.

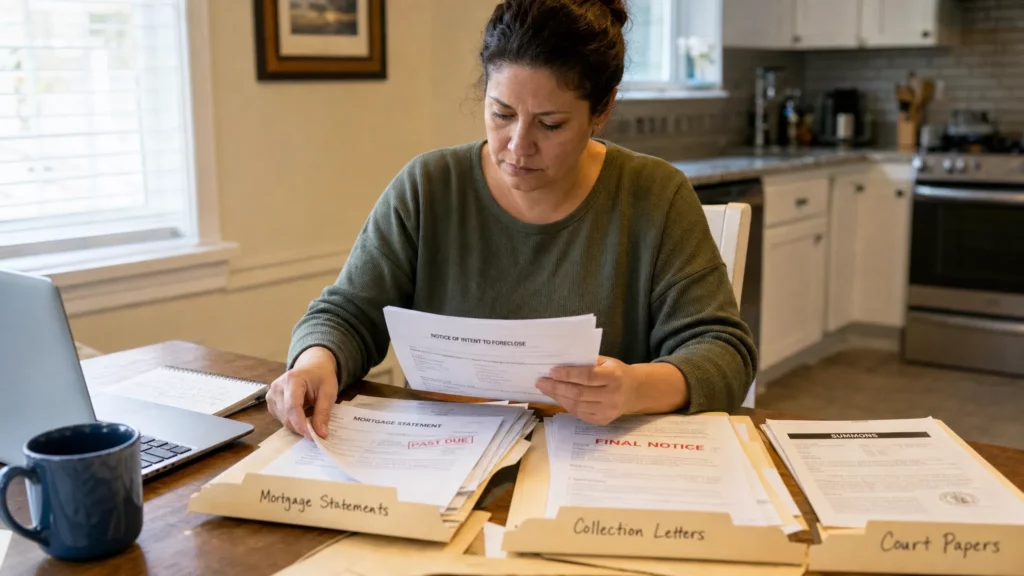

A debt collection lawsuit can feel overwhelming, especially when it arrives at the same time as missed mortgage payments, medical bills, credit card balances, or other financial pressure. Many New Yorkers assume that if a debt buyer or creditor has filed a case, the outcome is already decided. That is not true.

Debt collection attorneys who defend consumers can review whether the creditor has the right to sue, whether the lawsuit was filed on time, whether the amount claimed is accurate, and whether the collector followed New York and federal law. In many cases, consumers have more options than they realize, but the timing matters. Waiting too long can lead to default judgments, frozen bank accounts, wage garnishments, and added stress.

This article explains how consumer defense works in New York, what an attorney looks for, and why early action can make a meaningful difference.

What Debt Collection Attorneys Do for Consumers

Consumer debt defense is not simply about arguing that someone cannot afford to pay. It is about making sure the party suing can prove its case and that the consumer’s legal rights are protected throughout the process.

In New York, debt lawsuits may involve credit card balances, personal loans, medical debt, retail financing accounts, auto deficiency balances, or debts purchased by third-party debt buyers. A debt buyer may not be the original creditor. It may have purchased a portfolio of charged-off accounts, sometimes with limited documentation. That distinction matters because the plaintiff still has to prove ownership of the specific account and the amount allegedly owed.

A defense attorney may help by:

- Reviewing the summons, complaint, and supporting documents

- Determining whether the consumer was properly served

- Filing an answer before the deadline when appropriate

- Raising legal defenses and counterclaims

- Demanding proof through discovery

- Challenging defective affidavits or account records

- Negotiating settlements or payment terms

- Seeking to vacate default judgments when grounds exist

- Coordinating debt defense with bankruptcy or foreclosure defense when needed

The goal is not to create false hope or guarantee a dismissal. The goal is to make the creditor prove its case, protect the consumer from improper collection practices, and identify the most practical path forward.

Why Responding Quickly Matters in a New York Debt Lawsuit

A consumer debt case often begins with a summons and complaint. The papers may come from a creditor, a debt buyer, or a law firm collecting on behalf of a creditor. The complaint usually states that the consumer owes a certain amount and asks the court to enter judgment.

If the consumer does not respond, the creditor may ask the court for a default judgment. A judgment can create serious consequences. Depending on the circumstances, it may allow the creditor to pursue income executions, restrain bank accounts, or place a lien against real property in the county where the judgment is entered or docketed.

New York has strengthened protections for consumers in recent years. For example, the New York Consumer Credit Fairness Act changed important rules affecting consumer credit lawsuits, including time limits and documentation requirements. These protections can be valuable, but they usually must be raised properly and at the right time.

The most important first step is simple: do not ignore court papers. Even if you believe the debt is old, already paid, inflated, or not yours, failing to answer can make the case harder to defend later.

Common Defenses in New York Consumer Debt Cases

Every case is different, and no defense applies automatically. However, consumer debt collection attorneys commonly evaluate several issues before recommending a strategy.

| Defense issue | Why it matters | What an attorney may review |

| Improper service | A lawsuit may be defective if the consumer was not served according to New York rules | Affidavit of service, address used, method of delivery, timing |

| Statute of limitations | Some debts are too old to sue on | Date of last payment, charge-off date, account history, type of debt |

| Lack of standing | A debt buyer must prove it owns the specific debt | Assignment documents, bill of sale, account schedules, chain of title |

| Incorrect amount | Balances may include disputed fees, interest, or errors | Statements, payment records, interest calculations, settlement history |

| Insufficient proof | The plaintiff must support its claim with admissible evidence | Affidavits, account agreements, business records, witness knowledge |

| Identity or account dispute | The wrong person may be sued, or the account may involve fraud | Personal identifiers, account usage, credit reports, prior disputes |

| Collection law violations | Collectors must follow federal and state rules | Communications, threats, misrepresentations, harassment, notice issues |

Federal law also gives consumers rights. The Consumer Financial Protection Bureau explains that debt collectors generally may not use abusive, unfair, or deceptive practices, and consumers have rights when dealing with collectors under federal debt collection rules. You can review the CFPB’s overview of debt collection rights for general background.

These defenses are fact-sensitive. A consumer who has been sued should not assume that a debt is unenforceable just because it is old, sold to a debt buyer, or missing documents in the first mailing. At the same time, a consumer should not assume the plaintiff can prove everything it alleges.

How Attorneys Build a Debt Collection Defense

A strong defense usually starts with documents. The attorney reviews the court papers, account records, payment history, correspondence, and any collection notices the consumer received. If the case involves a debt buyer, the attorney may look closely at whether the assignment documents actually connect the plaintiff to the consumer’s specific account.

This document-focused approach is common in many civil disputes. Complex cases often turn on whether the claimant can organize and prove each disputed item. In construction litigation, for example, expert reports and Scott schedules are often used to clarify disputed work and costs, a process described by building consultants who support litigation. Consumer debt defense is a different area of law, but the broader lesson is similar: organized proof matters.

In a New York debt lawsuit, an attorney may file an answer denying allegations and asserting defenses. The attorney may then request documents through discovery, challenge the plaintiff’s evidence, appear in court conferences, and negotiate when appropriate. Sometimes the best result may be dismissal. In other cases, a practical settlement, affordable payment arrangement, or bankruptcy strategy may better serve the client’s long-term interests.

What If a Default Judgment Has Already Been Entered?

Many consumers first learn about a debt lawsuit after their bank account is frozen or their wages are threatened. This can happen when the creditor obtained a default judgment because the consumer did not answer the complaint.

A default judgment does not always end the matter. Depending on the facts, an attorney may consider whether there are grounds to ask the court to vacate the judgment. Common issues include improper service, lack of notice, excusable default, or a potentially valid defense to the case. The requirements depend on the circumstances, and timing can be important.

If a judgment is valid, the attorney may still explore options such as negotiating a reduced payoff, arranging payment terms, asserting exemption rights, or considering bankruptcy if the overall debt situation is unmanageable.

New York has also changed the financial impact of certain consumer debt judgments. The Fair Consumer Judgment Interest Act reduced the interest rate on qualifying consumer debt judgments, which can make a major difference for people facing old judgments that have grown over time.

Protecting Wages, Bank Accounts, and Property

A major reason to speak with a debt collection defense attorney is to understand what a judgment creditor can and cannot do. Collection threats often sound more absolute than the law allows.

For example, some income may be protected from garnishment, and certain funds in a bank account may be exempt from restraint depending on their source and amount. Social Security, public benefits, and other protected funds may require prompt action if they are frozen. A consumer should not assume that a bank restraint is lawful just because it occurred.

Homeowners have additional concerns. A debt judgment is different from a mortgage foreclosure, but it can still create risk if it becomes a lien against real estate. If you own a home and are also being sued for consumer debt, it is important to understand how debt lawsuits and foreclosure differ in New York so you can make informed decisions.

This is especially important for homeowners in Westchester County, Rockland County, Putnam County, Orange County, Dutchess County, the Bronx, and the Lower Hudson Valley, where home equity, mortgage arrears, and consumer debt problems can overlap. A strategy that handles only the collection lawsuit, without considering the home, may be incomplete.

Settlement Is Not Just About the Dollar Amount

Many debt cases resolve through settlement. However, a settlement should be reviewed carefully before signing. A low monthly payment may still create problems if the agreement includes harsh default terms, automatic judgment provisions, broad admissions, or unclear reporting obligations.

An attorney can help evaluate questions such as:

- Is the plaintiff able to prove the debt if the case continues?

- Is the settlement amount realistic based on income and expenses?

- Will the agreement result in a judgment, dismissal, or discontinuance?

- What happens if one payment is missed?

- Does the settlement resolve the full balance and related claims?

- Are there tax or credit reporting consequences to consider?

The right settlement depends on the strength of the defense, the consumer’s financial situation, and the risk of litigation. A settlement that works for one person may not work for another.

When Bankruptcy May Be Part of the Solution

Debt collection defense focuses on the lawsuit in front of you. Bankruptcy looks at the broader financial picture. For some consumers, defending one lawsuit is enough. For others, the lawsuit is only one symptom of a larger debt problem.

Chapter 7 bankruptcy may eliminate qualifying unsecured debts for eligible individuals. Chapter 13 bankruptcy may allow a person to reorganize debts over time, including mortgage arrears in some cases. Chapter 11 may be relevant for certain small business owners or individuals with more complex financial circumstances.

Bankruptcy can also trigger an automatic stay, which may stop many collection actions while the case is pending. That can be especially important for consumers facing wage garnishment, bank restraints, foreclosure pressure, or multiple creditor lawsuits. Bankruptcy is not right for everyone, and it should be evaluated carefully, but it is a legal financial tool, not a personal failure.

How to Choose a Debt Collection Defense Attorney in New York

When you are under pressure, it can be tempting to hire the first person who promises a fast result. Be careful. Debt collection defense should involve a realistic review of the documents, the court status, the amount at issue, and your broader financial goals.

Consider asking:

- Does the attorney regularly handle consumer debt defense in New York courts?

- Can they explain the lawsuit and deadlines in plain language?

- Will they review whether the plaintiff has standing and adequate proof?

- Can they evaluate settlement, litigation, and bankruptcy options together?

- Do they understand how a judgment may affect wages, bank accounts, and homeownership?

The best approach is usually practical and individualized. Some cases should be fought aggressively. Some should be settled carefully. Some require bankruptcy or a coordinated plan involving foreclosure defense, mortgage arrears, or other financial issues.

Frequently Asked Questions

Do I need an attorney if I really owe the debt? You may still benefit from legal advice. Even if a debt is valid, the plaintiff must follow proper procedures, prove the amount owed, and comply with applicable law. An attorney may also help negotiate terms that are more manageable.

Can a debt collector sue me after the statute of limitations expires? A time-barred debt may provide a defense, but you should not ignore the lawsuit. Statute of limitations issues must be analyzed based on the type of debt, payment history, and applicable New York law.

What happens if I missed the deadline to answer? You may still have options, especially if no judgment has been entered or if there were problems with service. If a default judgment already exists, an attorney can review whether there are grounds to ask the court to vacate it.

Can a creditor take my entire paycheck? Generally, wage garnishment is subject to legal limits, and some income may be protected. The exact analysis depends on your income, the type of debt, and whether a judgment has been entered.

Will bankruptcy stop a debt collection lawsuit? Bankruptcy may stop many collection actions through the automatic stay, depending on the circumstances. Whether bankruptcy is the right choice depends on your full financial situation, assets, income, debts, and goals.

Speak With a New York Consumer Debt Defense Attorney

If you have received a summons, collection notice, wage garnishment warning, bank restraint, or judgment paperwork, do not assume you are out of options. The earlier you seek guidance, the more time you may have to respond, raise defenses, protect exempt income, and evaluate settlement or bankruptcy alternatives.

Clair Gjertsen & Weathers PLLC helps New York consumers, homeowners, and families navigate debt lawsuits, foreclosure concerns, bankruptcy options, and related financial challenges. If you are facing a collection case in Westchester County, the Lower Hudson Valley, the Bronx, or the surrounding region, consider speaking with an experienced attorney before deadlines pass. Every case is unique, and a focused legal review can help you understand the path forward with greater clarity and confidence.

If you are overwhelmed by debt, behind on your mortgage, or worried about a lawsuit or wage garnishment, bankruptcy may feel like a last resort. In reality, bankruptcy is a legal tool designed to help individuals, families, and businesses regain control when debts become unmanageable.

So, do you need a lawyer for bankruptcies in New York? Legally, an individual can file bankruptcy without an attorney. Practically, many people benefit from legal guidance because a mistake can affect your home, car, bank account, foreclosure case, or ability to receive a discharge.

This is especially true in New York, where home values, foreclosure procedures, exemptions, court practices, and creditor claims can make bankruptcy more complicated than it first appears. The right question is not only whether you can file on your own. It is whether filing without counsel is worth the risk.

The short answer: You are not required to have a lawyer, but you may need one

Individuals are allowed to represent themselves in bankruptcy court. This is called filing pro se. However, bankruptcy is a federal court process with strict forms, deadlines, disclosure obligations, eligibility rules, and long-term consequences.

You should strongly consider speaking with a New York bankruptcy lawyer if any of the following apply:

- You own a home, condo, co-op, rental property, or valuable assets.

- You are behind on mortgage payments or facing foreclosure.

- You have been sued by a creditor or are facing wage garnishment.

- You are considering Chapter 13 to catch up on mortgage arrears.

- You have tax debt, student loans, domestic support obligations, or business debt.

- Your income changes from month to month or includes self-employment income.

- You recently transferred property, paid back relatives, or used retirement funds.

- You previously filed bankruptcy or had a case dismissed.

- You own a small business or personally guaranteed business debts.

A very simple no-asset Chapter 7 case may be easier to file without counsel than a case involving a home, foreclosure, business, or repayment plan. But even then, it is wise to understand the risks before submitting anything to the court.

What a bankruptcy lawyer does before you file

A bankruptcy attorney’s job is not simply to prepare forms. A good lawyer first helps you decide whether bankruptcy is the right option at all.

For some people, Chapter 7 bankruptcy may provide a clean path toward eliminating qualifying unsecured debts, such as credit cards or medical bills. For others, Chapter 13 may be better because it can create time to repay mortgage arrears, protect property, and manage debts over three to five years. In some cases, bankruptcy may not be the best first step, especially if a loan modification, foreclosure defense strategy, debt defense, settlement, or short sale should be considered.

Before filing, a bankruptcy lawyer typically reviews:

- Your income, expenses, assets, debts, and financial history.

- Whether you qualify for Chapter 7 under the means test.

- Whether Chapter 13 payments would be feasible.

- Whether your home equity is protected by exemptions.

- Whether a foreclosure sale, lawsuit, or garnishment creates urgent timing concerns.

- Whether any debts may be nondischargeable.

- Whether prior transfers or payments could create trustee issues.

This analysis matters because bankruptcy requires complete and accurate disclosure. Leaving out property, underestimating equity, misclassifying debt, or choosing the wrong chapter can create serious problems.

Chapter 7, Chapter 13, and Chapter 11 in plain English

The type of bankruptcy you file determines what happens next. The differences matter, particularly for New York homeowners and small business owners.

| Bankruptcy chapter | Common use | How it may help | Key caution |

| Chapter 7 | Individuals with limited income and mostly unsecured debt | May eliminate qualifying credit card debt, medical debt, and personal loans | Does not create a long-term plan to cure mortgage arrears, and nonexempt property may be at risk |

| Chapter 13 | Individuals with steady income who need time to repay certain debts | May help stop foreclosure, cure mortgage arrears, and protect assets through a court-approved plan | Requires regular plan payments, ongoing mortgage payments, and trustee approval |

| Chapter 11 | Businesses, some individuals with complex debts, and certain high-debt cases | May allow debt restructuring while operations continue | More complex and usually requires experienced counsel |

For many homeowners in Westchester County, Rockland County, Putnam County, Orange County, Dutchess County, the Bronx, and the Lower Hudson Valley, the decision often comes down to whether the primary goal is to eliminate unsecured debt, stop a foreclosure, or reorganize finances while keeping a home.

Why New York bankruptcy cases can be more complicated than they look

Bankruptcy law is federal, but local circumstances still matter. A case filed by a homeowner in White Plains, Yonkers, New Rochelle, the Bronx, or the Hudson Valley may involve local court practices, trustee expectations, New York foreclosure timelines, and New York property exemptions.

Many Lower Hudson Valley and Bronx bankruptcy cases are handled in the Southern District of New York, often through the bankruptcy court locations serving that region. The forms may be federal, but the way a trustee reviews income, expenses, mortgage arrears, real estate equity, and documentation can feel highly practical and fact-specific.

New York also allows debtors to choose between certain exemption systems, depending on the situation. Exemptions are laws that protect certain property from creditors and bankruptcy trustees. Choosing the wrong exemption approach can affect whether you can keep a home, vehicle, bank account, personal property, or potential claim.

That is one of the biggest reasons homeowners should be cautious about filing on their own. The question is not simply whether you own a home. It is how much equity exists, who owns the property, what liens are recorded, what exemption applies, and whether the chosen bankruptcy chapter protects your long-term goal.

Bankruptcy and foreclosure: Why timing is critical

For homeowners facing foreclosure, bankruptcy may provide immediate breathing room through the automatic stay. The automatic stay is a court order that generally stops most collection activity after a bankruptcy case is filed. Depending on the circumstances, it may temporarily stop a foreclosure sale, creditor lawsuit, wage garnishment, bank restraint, or collection calls.

However, the automatic stay is not a permanent solution by itself. A mortgage lender may ask the bankruptcy court for permission to continue foreclosure if the homeowner cannot make required payments, lacks a feasible Chapter 13 plan, or has filed multiple bankruptcy cases in a short period of time.

Chapter 13 can be especially useful for some New York homeowners because it may allow mortgage arrears to be repaid over three to five years while the homeowner resumes regular monthly mortgage payments. This can work alongside foreclosure defense, loss mitigation, or loan modification efforts, but it must be planned carefully.

Waiting until the night before a foreclosure auction can limit your options. Bankruptcy may still be possible in some urgent cases, but a rushed filing increases the risk of errors, missing documents, plan problems, or disputes over the automatic stay. Once a foreclosure sale has occurred, it may become much harder to protect the home.

Protecting your home, car, and other property

One of the most common fears about bankruptcy is losing everything. That is not how bankruptcy usually works, but property protection depends on the facts.

New York has homestead exemptions that may protect equity in a primary residence. The available protection can vary by county and is periodically adjusted. Westchester, Rockland, Putnam, Bronx, and New York City counties are generally in a higher New York homestead tier, while counties such as Dutchess and Orange may fall into a different tier. The correct amount should always be confirmed before filing.

Home equity is only one part of the analysis. A bankruptcy lawyer may also review:

- Whether the home is jointly owned.

- Whether there are judgment liens, tax liens, second mortgages, or HOA or condo arrears.

- Whether the mortgage balance and property value are accurate.

- Whether the homeowner should use New York exemptions or federal exemptions.

- Whether Chapter 7 or Chapter 13 better protects the property.

This is where filing without a lawyer can become dangerous. If a Chapter 7 trustee believes there is nonexempt equity, the trustee may investigate selling the property or negotiating a payment to the estate. In Chapter 13, nonexempt equity can affect how much must be paid to unsecured creditors through the plan.

Before transferring property, adding or removing someone from a deed, paying a relative, selling a car, or using retirement funds, speak with counsel. Actions taken shortly before bankruptcy can create issues that might have been avoided with early advice.

Bankruptcy and creditor lawsuits in New York

If a credit card company, debt buyer, medical creditor, or personal lender has sued you, bankruptcy may stop the lawsuit and prevent further collection activity while the case is pending. It may also discharge the underlying debt if the debt qualifies.

But bankruptcy does not erase every type of debt. Some obligations may survive bankruptcy or require additional litigation. These can include certain taxes, domestic support obligations, many student loans, criminal restitution, and debts connected to fraud or intentional misconduct.

A lawyer can help determine whether the debt is dischargeable, whether the creditor has a valid claim, and whether bankruptcy is better than defending the lawsuit in state court. This is particularly important if a creditor already has a judgment, has restrained a bank account, or is garnishing wages.

Small businesses and bankruptcy counsel

Small business owners often face a mix of personal and business debt. A business loan may be personally guaranteed. A landlord may be pursuing rent. Vendors may be demanding payment. Tax debt, payroll obligations, equipment leases, and merchant cash advances can all overlap.

If you operate a corporation or LLC, the legal analysis becomes more complex. Business entities generally cannot represent themselves in federal court the same way an individual can. Chapter 11, including Subchapter V for qualifying small business debtors, typically requires experienced legal guidance.

A business bankruptcy lawyer can help evaluate whether the goal is to close down, reorganize, sell assets, negotiate with creditors, or continue operations. For businesses whose value includes copyrights, trademarks, licensing rights, or other intangible assets, broader asset planning may also matter. In that setting, resources such as IP monitoring and licensing tools may be part of understanding potential revenue streams, while bankruptcy counsel focuses on how those assets and contracts are treated in a restructuring.

What can go wrong if you file bankruptcy without legal help?

Bankruptcy paperwork can seem straightforward at first because many forms ask for basic financial information. The difficulty is knowing the legal effect of each answer.

| Potential mistake | Why it matters |

| Filing the wrong chapter | You may lose protection you needed or end up in a plan you cannot afford |

| Miscalculating home equity | Nonexempt equity can create risk in Chapter 7 or increase Chapter 13 payments |

| Leaving out a creditor | Notice problems can affect discharge and case administration |

| Failing the means test | A Chapter 7 case may be challenged or dismissed |

| Missing required courses or documents | The case may be delayed, dismissed, or closed without discharge |

| Ignoring secured debts | Mortgage, car loan, co-op, condo, and tax issues may continue after discharge |

| Filing too late before a foreclosure sale | Emergency filings can be incomplete, and options may be narrower |

A dismissed bankruptcy case can also make future filings harder, especially if there are repeated cases and questions about the automatic stay. That is why early legal advice often creates more room to plan.

When filing without a lawyer may be more realistic

There are situations where a person may decide to file without an attorney. For example, someone with low income, no real estate, no valuable assets, no recent transfers, no lawsuits involving disputed debts, and only basic unsecured debt may have a more straightforward Chapter 7 case.

Even then, the person must complete credit counseling, prepare accurate schedules, attend the 341 meeting of creditors, cooperate with the trustee, take the required financial management course, and understand what debts will and will not be discharged.

The simpler the case, the more realistic self-filing may be. The more you have to protect, the more important legal advice becomes.

Questions to ask a New York bankruptcy lawyer

Before hiring counsel, you should feel comfortable asking direct questions. A good consultation should leave you with a clearer understanding of your options, not more confusion.

Consider asking:

- Do I qualify for Chapter 7, Chapter 13, or another option?

- How will bankruptcy affect my home, car, bank accounts, and wages?

- Can bankruptcy stop my foreclosure sale or creditor lawsuit?

- What debts are likely to be discharged, and what debts may remain?

- Are there non-bankruptcy options I should consider first?

- What documents do you need to review before recommending a strategy?

- What deadlines should I be worried about right now?

If you are a homeowner, bring mortgage statements, foreclosure papers, loan modification correspondence, tax bills, and any sale notices. If you are dealing with lawsuits or garnishments, bring the summons, complaint, judgment, wage garnishment notice, or bank restraint paperwork.

Bankruptcy is not failure. It is a legal path toward stability

Many people delay speaking with a lawyer because they feel embarrassed or believe bankruptcy means they have failed. Financial hardship can happen for many reasons, including job loss, illness, divorce, business disruption, medical bills, rising housing costs, or the end of a mortgage forbearance.

Bankruptcy exists because the law recognizes that people and businesses sometimes need structured relief. The goal is not punishment. The goal is to create an orderly process for dealing with debt and, when possible, giving honest debtors a fresh start.

The key is choosing the right strategy. For one person, that may mean Chapter 7. For another, it may mean Chapter 13, a loan modification, foreclosure defense, settlement, short sale, or a combination of approaches.

Frequently Asked Questions

Do I legally need a lawyer to file bankruptcy in New York? Individuals are generally allowed to file bankruptcy without a lawyer, but it can be risky. If you own a home, face foreclosure, have lawsuits, own a business, or have valuable assets, legal guidance is strongly recommended.

Can a bankruptcy lawyer help stop foreclosure? Bankruptcy may stop or delay a foreclosure through the automatic stay if filed before the sale, depending on the circumstances. Chapter 13 may also allow some homeowners to cure mortgage arrears over time, but the plan must be feasible.

Is Chapter 7 or Chapter 13 better for New York homeowners? It depends on your income, home equity, mortgage arrears, and goals. Chapter 7 may help with unsecured debt, while Chapter 13 is often more useful when a homeowner needs time to catch up on missed mortgage payments.

Will I lose my house if I file bankruptcy? Not necessarily. Many people keep their homes in bankruptcy, but protection depends on equity, exemptions, mortgage status, liens, and the chapter filed. A lawyer can evaluate the risk before you file.

How much does a bankruptcy lawyer cost? Fees vary based on the chapter, urgency, complexity, and whether foreclosure, litigation, business debt, or asset issues are involved. Ask for a clear written fee agreement and make sure you understand what services are included.

Should I wait until a foreclosure auction is scheduled before calling a lawyer? No. Waiting can reduce your options. Early advice may allow time to explore foreclosure defenses, loan modification, Chapter 13, loss mitigation, or other strategies before deadlines become urgent.

Speak with a New York bankruptcy and foreclosure attorney before deadlines pass

If you are considering bankruptcy in Westchester County, Rockland County, Putnam County, Orange County, Dutchess County, the Bronx, or the Lower Hudson Valley, you do not have to make the decision alone.

Clair Gjertsen & Weathers PLLC helps homeowners, consumers, landlords, tenants, and small businesses evaluate practical legal options during financial stress. Whether you are facing foreclosure, creditor lawsuits, wage garnishment, overwhelming debt, or uncertainty about Chapter 7, Chapter 13, or Chapter 11, experienced counsel can help you understand your rights and avoid preventable mistakes.

Every case is unique, and no outcome can be guaranteed. But the earlier you seek advice, the more options you may have. If you are worried about debt or your home, contact Clair Gjertsen & Weathers PLLC to discuss your situation and determine the next step that may best protect your future.

Financial pressure can make a business owner feel trapped. Vendors want payment, a landlord may be threatening legal action, lenders may be calling daily, and cash flow may not be enough to cover payroll, rent, taxes, and debt service. In that moment, bankruptcy can sound like the end of the company. In many cases, however, it is better understood as a legal tool that may create time, structure, and leverage.

A business bankruptcies attorney, more commonly called a business bankruptcy attorney, may help determine whether a company can reorganize, negotiate with creditors, sell assets in an orderly way, or protect the owner from unnecessary personal exposure. The key is timing. The earlier a business owner seeks advice, the more options may be available.

For small businesses in Westchester County, the Bronx, the Lower Hudson Valley, and surrounding New York communities, bankruptcy decisions often overlap with real estate, leases, personal guarantees, tax obligations, foreclosure risk, and consumer debt. That is why the analysis should be practical, not one-size-fits-all.

What a business bankruptcy attorney actually does

A business bankruptcy attorney does more than file forms with the court. The attorney’s first job is to understand whether the business has a viable path forward.

That analysis usually includes cash flow, creditor pressure, pending lawsuits, tax debt, secured loans, equipment financing, leases, contracts, accounts receivable, payroll obligations, and the owner’s personal guarantees. For closely held businesses, the attorney may also need to review how business debt affects the owner’s home, bank accounts, wages, or other personal assets.

In plain terms, the question is not simply, “Can this company file bankruptcy?” The more important question is, “What legal strategy gives this business the best chance to preserve value, reduce pressure, and move forward?”

Sometimes the answer is Chapter 11 reorganization. Sometimes it is Subchapter V, a streamlined Chapter 11 option for eligible small business debtors. Sometimes it is a negotiated workout outside of bankruptcy. In other cases, an orderly shutdown or sale may protect more value than a chaotic creditor race.

Warning signs that a business should seek bankruptcy counsel

Many business owners wait too long because they believe the next contract, busy season, refinance, or investor will solve the problem. Sometimes it does. But when legal deadlines and creditor actions begin piling up, delay can reduce available choices.

A business owner should consider speaking with counsel if any of the following are happening:

- The company is behind on rent, mortgage payments, payroll taxes, or sales taxes.

- A creditor has filed a lawsuit or obtained a judgment.

- A bank account has been restrained or frozen.

- A landlord has served a default notice, notice to cure, or termination notice.

- A secured lender is threatening repossession of vehicles, equipment, or inventory.

- Merchant cash advance payments or daily withdrawals are draining operating cash.

- The business is using new debt to pay old debt without a realistic turnaround plan.

- The owner has personally guaranteed business loans and is receiving demand letters.

- The company cannot keep up with payroll or essential vendors.

These signs do not automatically mean bankruptcy is required. They do mean the business should be evaluated before creditors make decisions for it.

How bankruptcy can create breathing room

One of the most powerful features of bankruptcy is the automatic stay. In many cases, the automatic stay takes effect immediately when a bankruptcy petition is filed. It can pause collection lawsuits, judgment enforcement, bank restraints, repossessions, foreclosure activity, and other creditor actions.

For a struggling business, that pause can be critical. It may allow management to stabilize operations, review contracts, negotiate with lenders, and propose a repayment or restructuring plan under court supervision.

The automatic stay is not unlimited. Certain tax, regulatory, criminal, eviction, and repeat-filing issues may be treated differently depending on the circumstances. A business may also need court permission to use cash collateral, obtain financing, assume or reject leases, or sell significant assets. This is why experienced legal guidance matters.

Bankruptcy is not just about stopping creditors. It is about using the time created by the stay to pursue a realistic business outcome.

Which bankruptcy chapter may apply to a business?

The right bankruptcy chapter depends on the company’s structure, revenue, debts, goals, and whether the business intends to continue operating. The table below provides a simplified overview.

| Bankruptcy option | Who may use it | Common purpose | Important considerations |

| Chapter 11 | Corporations, LLCs, partnerships, and individuals | Reorganize debt while continuing operations | More complex, involves court oversight, plans, reporting, and creditor treatment rules |

| Subchapter V of Chapter 11 | Eligible small business debtors | Streamlined small business reorganization | Debt limits and eligibility rules apply; often designed to move faster than traditional Chapter 11 |

| Chapter 7 business liquidation | Businesses that are closing or cannot reorganize | Liquidate assets through a trustee | Corporations and LLCs generally do not receive a discharge, but liquidation may bring order to creditor claims |

| Chapter 13 | Individuals with regular income, including some sole proprietors | Repay debts over time while keeping assets | Not available to corporations or LLCs; may help an individual owner address personal and business-related debt |

For individuals and small business owners trying to understand the broader bankruptcy landscape, CGW’s guide to filing bankruptcy in Westchester County and the Hudson Valley provides additional context about how bankruptcy may work for local residents.

When bankruptcy may actually save a company

Bankruptcy is most likely to help preserve a business when there is a viable core operation. That means the company can potentially operate profitably if creditor pressure, lawsuits, arrears, or unsustainable debt terms are addressed.

For example, a contractor, restaurant, retail shop, medical practice, professional office, or service company may have loyal customers and meaningful revenue but be overwhelmed by past-due rent, tax debt, litigation, high-interest loans, or equipment financing. A cash-flow crisis can affect even practical, demand-driven businesses, from a neighborhood restaurant to a plumbing and drain service that depends on vehicles, tools, staffing, supplies, and rapid response to keep income moving.

A business bankruptcy attorney may help save a company in several common situations.

The business has revenue but old debt is suffocating it

A company can be operationally sound and still be financially distressed. Past-due obligations may consume so much cash that the business cannot buy inventory, pay employees, maintain equipment, or accept new work.

A reorganization may allow the business to separate ongoing operating expenses from older debt. The company may be able to propose a plan to repay creditors over time, restructure secured debt, address lease arrears, and continue serving customers.

A lawsuit or judgment threatens to shut down operations

A single judgment creditor can create serious disruption. Bank restraints, income executions, liens, and enforcement actions can make it impossible to run payroll or pay vendors. Bankruptcy may stop the race among creditors and bring disputes into one forum.

For owners who personally guaranteed business debts, creditor lawsuits may also create personal risk. CGW has discussed related issues in the context of how to protect your home from debt lawsuits in New York, and business owners should take personal exposure seriously before judgments are entered or enforced.

The business needs time to deal with a commercial lease

For many New York businesses, the lease is central to survival. A restaurant, storefront, warehouse, office, or professional practice may not be able to relocate quickly. If the company is behind on rent or has received a default notice, a bankruptcy filing may create time to evaluate whether the lease can be assumed, rejected, renegotiated, or addressed through a plan.

Commercial lease issues are time-sensitive in bankruptcy. Post-filing rent obligations and statutory deadlines can move quickly. Waiting until after a warrant, lockout, or termination may significantly complicate the situation.

The company needs to sell assets without a creditor scramble

Sometimes saving the business does not mean keeping the exact same ownership structure or operations. A bankruptcy case may allow a company to sell assets in an orderly process, preserve going-concern value, and avoid piecemeal creditor seizures.

This can matter where equipment, licenses, contracts, customer lists, real estate, or inventory have more value together than they would in a forced liquidation.

The owner needs a coordinated personal and business debt strategy

Many small businesses are closely connected to the owner’s personal finances. The owner may have signed personal guarantees, used personal credit cards, pledged a home, or fallen behind on household bills while trying to keep the company alive.

In those cases, the attorney may need to consider both business bankruptcy and personal bankruptcy options. CGW’s Consumer Bankruptcy 101 explains some basic differences between Chapter 7 and Chapter 13 for individuals, which may be relevant when a sole proprietor or guarantor is facing personal liability.

Chapter 11 and Subchapter V: what “saving the company” can look like

In a Chapter 11 case, the business generally seeks to reorganize while continuing operations. Management may remain in control as a debtor in possession, subject to bankruptcy court oversight. The company may seek permission to pay essential expenses, use cash collateral, obtain financing, sell assets, reject burdensome contracts, and propose a plan for creditor repayment.

Subchapter V was created to make Chapter 11 more accessible for eligible small business debtors. It can reduce some of the cost and complexity associated with traditional Chapter 11, although eligibility rules, debt limits, reporting duties, and court deadlines still matter.

A successful reorganization may involve:

- Paying priority taxes over time when legally permitted.

- Restructuring secured debt based on asset value and plan requirements.

- Catching up lease or loan arrears through a structured plan.

- Rejecting contracts that drain the business.

- Selling nonessential assets to fund operations or creditor payments.

- Negotiating with creditors under court supervision.

No attorney can guarantee that a bankruptcy plan will be confirmed or that a company will survive. Creditors, cash flow, court requirements, tax issues, and management decisions all matter. But in the right circumstances, bankruptcy can replace panic-driven creditor pressure with an organized legal process.

When bankruptcy may not be the right answer

A responsible attorney should also tell a business owner when bankruptcy may not solve the problem. If the company has no realistic revenue, no ability to pay ongoing expenses, no viable market, or no path to compliance with tax and regulatory obligations, reorganization may not be practical.

Bankruptcy may also be less helpful if the main issue is a dispute that can be resolved through negotiation, litigation defense, refinancing, a landlord agreement, or a sale outside of bankruptcy.

In some cases, alternatives may include creditor workouts, lease negotiations, business asset sales, real estate transactions, payment agreements, or an orderly wind-down. The best option depends on the facts, and it should be evaluated before the business runs out of cash, loses its location, or faces enforcement actions that are harder to reverse.

What to prepare before meeting with a business bankruptcy attorney

A productive consultation depends on accurate information. Business owners do not need to have everything perfectly organized, but they should gather enough documents to allow meaningful analysis.

Helpful materials include recent profit and loss statements, balance sheets, tax returns, bank statements, loan documents, leases, lawsuits, judgments, UCC filings, equipment finance agreements, merchant cash advance agreements, payroll tax notices, sales tax notices, accounts receivable reports, accounts payable lists, and any personal guarantee documents.

It is also important to be honest about goals. Does the owner want to save the company, sell it, close it, protect a home, stop a lawsuit, keep employees, preserve a license, or negotiate with a landlord? The legal strategy should be built around realistic goals, not assumptions.

Mistakes that can reduce business bankruptcy options

Many business owners make decisions under pressure that feel necessary in the moment but create problems later. Before moving money, selling assets, paying insiders, or signing new agreements with aggressive creditors, it is wise to get legal advice.

Common mistakes include paying family members or insiders ahead of other creditors, using trust fund taxes for operating expenses, ignoring lawsuit deadlines, transferring assets without fair value, taking high-cost financing without understanding the terms, signing confessions of judgment where applicable, and waiting until the day before a lockout, auction, or account restraint.

The earlier a business owner seeks advice, the more room there may be to plan. Waiting does not always eliminate options, but it often makes every option more expensive and more urgent.

Frequently Asked Questions

Can an LLC file Chapter 13 bankruptcy? No. Chapter 13 is available only to individuals with regular income, not corporations or LLCs. An LLC may need to consider Chapter 11, Subchapter V if eligible, Chapter 7 liquidation, or non-bankruptcy alternatives.

Does business bankruptcy mean the company must close? Not always. Chapter 11 and Subchapter V are designed to allow eligible businesses to reorganize while continuing operations, depending on cash flow, creditor issues, court requirements, and the company’s ability to propose a workable plan.

Can bankruptcy stop a business eviction in New York? It may help in some situations, but timing and lease status are critical. Commercial lease rights can change quickly after defaults, termination notices, warrants, and missed post-filing rent obligations. A business should seek advice as early as possible.

Will a business bankruptcy protect the owner personally? It depends. If the owner personally guaranteed debts, pledged personal assets, or owes related tax obligations, a business filing alone may not fully protect the owner. A coordinated personal and business debt analysis may be necessary.

Is Subchapter V always better than regular Chapter 11? Not always. Subchapter V can be a powerful option for eligible small businesses, but eligibility rules, debt limits, creditor issues, and case strategy matter. An attorney can help determine whether it fits the company’s situation.

Speak with a New York business bankruptcy attorney before options narrow

If your business is facing lawsuits, lease defaults, creditor pressure, tax problems, foreclosure risk, or overwhelming debt, you do not have to make decisions in the dark. Bankruptcy may or may not be the right answer, but understanding your options early can make a significant difference.

Clair Gjertsen & Weathers PLLC helps business owners, homeowners, and consumers in Westchester County, the Bronx, the Lower Hudson Valley, and surrounding New York communities evaluate practical legal strategies for debt, bankruptcy, foreclosure, and property-related disputes.

Every case is unique. If your company is under financial pressure, consider speaking with experienced counsel before deadlines pass, assets are seized, or creditors gain more leverage.

Many people search for a bankruptcies lawyer when the bills, collection calls, court papers, or mortgage arrears become too much to manage alone. The better term is bankruptcy lawyer, but the concern behind the search is clear: you need to know whether the law can give you breathing room, and you need to choose someone you can trust.

Bankruptcy is not right for everyone. It is also not a personal failure. For many New York consumers, homeowners, and small business owners, bankruptcy can be a practical legal tool for stopping creditor pressure, reorganizing debt, protecting wages, and, in some cases, creating a path to keep a home.

Before hiring an attorney, it helps to understand what a good bankruptcy consultation should cover, what questions to ask, and what warning signs to avoid.

Bankruptcy is a legal tool, not a last-resort label

The U.S. Courts describe bankruptcy as a legal process that helps people and businesses who cannot repay debts. That process can be powerful, but it must be used carefully.

One of the most important protections is the automatic stay. In many cases, once a bankruptcy petition is filed, the automatic stay temporarily stops collection activity. Depending on the circumstances, this may pause wage garnishments, creditor lawsuits, collection calls, bank restraints, repossessions, and foreclosure activity.

That does not mean bankruptcy erases every problem or guarantees that a home, car, or business will be saved. A good bankruptcy lawyer should explain both the benefits and the limits. The goal is not simply to file a case. The goal is to choose the right strategy for your financial reality.

When should you speak with a bankruptcy lawyer?

Many people wait until the situation feels unbearable. Unfortunately, waiting can reduce available options, especially if a foreclosure sale, wage garnishment, eviction, or creditor judgment is already moving forward.

You should consider speaking with a bankruptcy lawyer if:

- You are behind on mortgage payments and have received foreclosure papers.

- You have a scheduled foreclosure auction or fear one may be coming.

- You are being sued by a credit card company, debt buyer, lender, or medical creditor.

- Your wages are being garnished or your bank account has been restrained.

- You cannot keep up with credit cards, personal loans, medical bills, or tax obligations.

- You are a landlord, small business owner, or self-employed person facing business-related debt.

- You are considering a debt settlement program but are unsure whether it is safe or realistic.

Bankruptcy is often most effective when it is evaluated before deadlines pass. Even if you ultimately decide not to file, a consultation can help you understand your legal position.

Understand which type of bankruptcy may apply

Not all bankruptcies work the same way. The chapter that fits one person may be completely wrong for another. A responsible attorney should explain the differences in plain language and connect the recommendation to your goals.

| Bankruptcy chapter | Common purpose | Why it may matter |

| Chapter 7 | Liquidation bankruptcy for qualifying individuals or businesses | May eliminate many unsecured debts, such as credit cards and medical bills, but asset protection must be carefully reviewed. |

| Chapter 13 | Repayment plan for individuals with regular income | May help homeowners catch up on mortgage arrears over time while maintaining ongoing payments. |

| Chapter 11 | Reorganization for businesses and certain individuals with complex debts | May allow a business to restructure debt while continuing operations, depending on the facts. |

For many consumers, the choice is between Chapter 7 and Chapter 13. Chapter 7 may be appropriate for someone with limited income and mostly unsecured debt. Chapter 13 may be more useful for a homeowner who has fallen behind on mortgage payments but has enough income to make ongoing payments and a court-approved plan payment.

If you are unsure where you fit, you may find it helpful to review CGW’s guide on Chapter 7 vs. Chapter 13 bankruptcy in Westchester and the Hudson Valley. Still, your own situation should be reviewed by an attorney before you make decisions.

Why New York bankruptcy experience matters

Bankruptcy is federal law, but local practice still matters. For many residents of Westchester, Rockland, Putnam, Orange, Dutchess, and Bronx Counties, bankruptcy cases are handled in the U.S. Bankruptcy Court for the Southern District of New York, including the White Plains division depending on venue.

A lawyer familiar with New York practice should understand local procedures, trustee expectations, foreclosure timing, state court litigation, and the interaction between bankruptcy and New York property rights. This can be especially important for homeowners.

New York residents must also carefully evaluate exemptions. Exemptions are laws that may protect certain property in bankruptcy, such as equity in a home, a vehicle, retirement funds, household goods, or other assets. In New York, debtors may often need to compare New York exemptions and federal exemptions, but they generally cannot mix and match between systems. The better choice depends on the property you own, the equity you have, and your overall goals.

This is one reason a quick form-based filing or one-size-fits-all approach can be risky. Small details can have major consequences.

What a bankruptcy lawyer should review before recommending a filing

A bankruptcy lawyer should not recommend filing based only on your total debt. The attorney should look at your full financial picture, including your income, assets, household expenses, secured debts, lawsuits, tax history, and property transfers.

Before or during your consultation, try to gather:

- Recent pay stubs, profit and loss information, or other income records.

- Mortgage statements, foreclosure notices, and court papers.

- Credit card bills, medical bills, personal loan statements, and collection letters.

- Tax returns, tax notices, and information about any unpaid taxes.

- Bank statements and retirement account statements.

- Vehicle loan statements, leases, and title information.

- Any lawsuits, judgments, wage garnishment notices, or bank restraint documents.

The lawyer should ask about recent payments to relatives, property transfers, refinancing, business interests, prior bankruptcies, and expected changes in income. These questions are not meant to judge you. They help the attorney spot risks before they become problems.

Questions to ask before hiring a bankruptcy lawyer

The right lawyer should welcome practical questions. You are not just hiring someone to prepare forms. You are hiring someone to help you evaluate risk, timing, and strategy during a stressful financial period.

| Question to ask | Why it matters |

| Have you handled cases like mine? | A homeowner facing foreclosure has different concerns than someone with only credit card debt. |

| Which chapter do you believe may fit my situation, and why? | The answer should be tied to your income, assets, debts, and goals. |

| What are the risks of filing? | Every bankruptcy case has potential downsides, including asset, credit, timing, or eligibility issues. |

| How will bankruptcy affect my home, car, wages, or business? | Secured property and income issues need careful review before filing. |

| Are there non-bankruptcy options I should consider? | Bankruptcy may be one option among foreclosure defense, loan modification, settlement, or debt defense. |

| What fees and costs should I expect? | You should understand attorney fees, court filing fees, required courses, and what services are included. |

| Who will handle my case day to day? | Clear communication matters, especially when deadlines are involved. |

| What deadlines should I be worried about right now? | Foreclosure sales, answer deadlines, garnishments, and court dates may require immediate action. |

A clear attorney-client relationship should include a written retainer agreement that explains the scope of representation. If you do not understand what is included, ask before signing.

Warning signs to watch for

Most bankruptcy lawyers are serious professionals, but consumers in financial distress can be vulnerable to poor advice. Be cautious if someone treats bankruptcy like a quick transaction without reviewing your documents or goals.

Warning signs may include:

- Promises that all debts will definitely disappear.

- Guarantees that you will keep your home or stop foreclosure permanently.

- Pressure to sign immediately without time to ask questions.

- Vague or changing fee explanations.

- Advice to hide assets, transfer property, or leave information out of court documents.

- A refusal to discuss alternatives or risks.

- A non-lawyer company offering legal advice about foreclosure, debt, or bankruptcy.

Bankruptcy petitions are signed under penalty of perjury. Accuracy matters. A lawyer should help you disclose information properly, not avoid disclosure.

Fees are important, but cheapest is not always safest

Cost matters when you are already under financial pressure. You should absolutely ask about fees, payment arrangements, court costs, and what services are included. At the same time, the lowest advertised fee may not be the best value if the lawyer does not review your home equity, foreclosure status, tax issues, prior filings, business interests, or lawsuit deadlines.

A poorly planned bankruptcy can lead to dismissal, loss of protection, unnecessary litigation, or avoidable stress. In a Chapter 13 case, an unrealistic plan can fail if the monthly payment does not match your actual budget. In a Chapter 7 case, failing to analyze assets and exemptions can create serious problems.

The right question is not only, how much does it cost? It is also, what legal analysis am I receiving for that cost?

If you own a home, bankruptcy and foreclosure strategy must be coordinated

For New York homeowners, bankruptcy may overlap with foreclosure defense, loan modification, loss mitigation, short sale planning, or post-judgment strategy. Filing bankruptcy without coordinating it with the foreclosure case can cause confusion or missed opportunities.

For example, Chapter 13 may help some homeowners spread mortgage arrears over a repayment plan while they resume regular mortgage payments. In other situations, bankruptcy may provide temporary breathing room while the homeowner evaluates a loan modification, sale, settlement, or other option. Chapter 7 may stop collection activity for a time, but it usually does not create a long-term mortgage arrears repayment plan.

Timing is especially important if a foreclosure auction has already been scheduled. The automatic stay can be powerful, but prior bankruptcy cases, repeat filings, motions for relief from stay, or post-sale issues can affect what protection is available. Every case is unique.

CGW has written more about this issue in When Foreclosure and Bankruptcy Overlap for New York Homeowners and How Chapter 13 Bankruptcy Can Help Stop Foreclosure in NY. If you are facing foreclosure, do not assume it is too early or too late to ask for help. Options may still exist, but they often depend on timing.

What to do before your first consultation

You do not need to have everything perfectly organized before contacting a lawyer. Still, a little preparation can make the consultation more productive.

Before you meet with an attorney:

- Open and save all court papers, foreclosure notices, collection letters, and lender mail.

- Write down key dates, including court appearances, sale dates, default notices, and garnishment dates.

- Make a rough list of debts, assets, income, and monthly expenses.

- Avoid transferring property, repaying relatives, or draining retirement accounts without legal advice.

- Be honest about prior bankruptcies, lawsuits, tax debt, and property ownership.

If there is an urgent deadline, tell the attorney immediately when you call. A foreclosure auction, eviction date, wage garnishment, or lawsuit answer deadline can change the priority of the legal strategy.

What happens after you hire a bankruptcy lawyer?

After you hire a lawyer, the next steps depend on the type of case and your goals. Typically, the attorney will collect documents, analyze eligibility, review exemptions, identify risks, and advise whether bankruptcy or another option makes sense.

If bankruptcy is appropriate, you may need to complete required credit counseling before filing. Your lawyer will prepare the bankruptcy petition, schedules, statements, and related documents. These papers disclose your debts, assets, income, expenses, transfers, and financial history.

Once the case is filed, the automatic stay generally goes into effect, subject to important exceptions. You will also attend a meeting of creditors, often called a 341 meeting, where a trustee asks questions about your filing. In Chapter 13, you must also propose and maintain a repayment plan. In Chapter 7, the case may move toward discharge if there are no objections or complications.

A good lawyer should keep you informed about what to expect, what you must provide, and what deadlines matter.

Frequently Asked Questions

Do I really need a lawyer to file bankruptcy? Individuals can file without an attorney, but bankruptcy is document-heavy and mistakes can be costly. If you own a home, face foreclosure, have significant assets, owe taxes, operate a business, or have been sued, legal guidance is especially important.