NY & CT Foreclosure & Bankruptcy Attorneys

Schedule A Free Consultation 914.472.6202

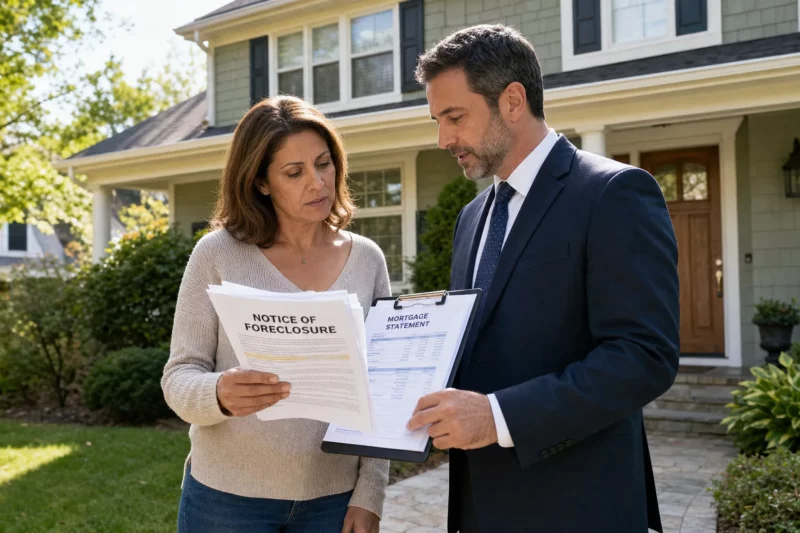

If you are behind on your mortgage or have been served with foreclosure papers, it is natural to feel like time has already run out. In New York, however, foreclosure is a court process. That means the lender must follow specific rules, and homeowners often have opportunities to respond, negotiate, defend the case, or explore alternatives before losing the home.

A foreclosure attorney in New York can help at several points, from the first missed payments to a scheduled auction or even certain post-sale situations. The earlier you seek guidance, the more options may be available, but late-stage cases can still deserve careful review.

This article explains when legal help can make a meaningful difference, what an attorney may look for, and how homeowners in Westchester County, the Bronx, Rockland, Putnam, Orange, Dutchess, and the Lower Hudson Valley can begin protecting their rights.

New York Foreclosure Is a Court Case, Not Just a Bank Decision

New York is a judicial foreclosure state. In most residential mortgage cases, the lender cannot simply change the locks or sell the property without first filing a lawsuit in New York Supreme Court, which is the trial-level court in New York.

That court process matters. It gives homeowners the right to receive proper notices, answer the lawsuit, raise defenses, participate in settlement conferences if eligible, challenge improper documents, and ask the court for relief in appropriate circumstances.

The New York State Unified Court System provides general foreclosure information for homeowners, but every case depends on the mortgage documents, payment history, notices, court filings, prior litigation, and the homeowner’s financial goals. An experienced attorney can connect those pieces and help determine whether the home can be saved, the case can be defended, or another solution makes more sense.

Quick Answer: When Can a Foreclosure Attorney Help Save a Home?

A foreclosure attorney may be able to help whenever a homeowner is at risk of losing the property, not only after a lawsuit is filed. The strategy changes depending on the stage of the case.

| Stage of the problem | What may be happening | How an attorney may help |

|---|---|---|

| Missed payments | You are behind but have not received legal papers | Review options, communicate with the servicer, prepare for loss mitigation, and help avoid mistakes |

| 90-day notice | You received a New York pre-foreclosure notice | Check whether the notice complies with New York law and begin planning a defense or modification strategy |

| Summons and complaint | A foreclosure lawsuit has started | File an answer, assert defenses, review service, and protect you from defaulting in the case |

| Settlement conference | The court schedules conferences with the lender | Advocate for a loan modification or other resolution and hold the servicer accountable |

| Motion or judgment stage | The lender asks the court for judgment | Oppose improper motions, challenge amounts claimed, and preserve defenses |

| Auction scheduled | A sale date has been set | Evaluate emergency options such as a stay, bankruptcy, reinstatement, payoff, short sale, or other relief |

| After foreclosure sale | The property has been sold and eviction may follow | Review whether any limited challenges, surplus issues, occupancy agreements, or bankruptcy questions remain |

The most important point is this: do not assume that one notice, one missed deadline, or one denial of a loan modification means nothing can be done. It may be harder to fix a problem later, but the case should be reviewed before you decide there are no options.

Before a Foreclosure Lawsuit: Missed Payments and the 90-Day Notice

Many homeowners first contact a lawyer after receiving a “90-day notice.” In New York, RPAPL 1304 generally requires a lender or servicer to send a specific pre-foreclosure notice before starting many residential foreclosure actions. The notice is intended to give homeowners time to seek help, contact housing counselors, and explore alternatives.

This is often one of the best times to speak with counsel. At this stage, there may not yet be a court case, but the risk is real. A lawyer can review the loan, explain the likely timeline, and help the homeowner avoid common mistakes such as submitting incomplete modification packages, ignoring servicer requests, or making informal agreements without written confirmation.

A foreclosure attorney can also examine whether the required notice appears legally sufficient. New York courts have taken pre-foreclosure notice requirements seriously, and notice defects may become important defenses if the lender later files a lawsuit.

If you are still in the pre-lawsuit stage, options may include applying for a loan modification, requesting repayment or deferral options, reinstating the loan if funds are available, selling the property, or preparing for a legal defense if foreclosure is filed. CGW has more information on how homeowners may apply for a loan modification when they are trying to avoid foreclosure.

After You Are Served: The Answer Deadline Is Critical

Being served with a summons and complaint is a major turning point. It means the lender has started a foreclosure lawsuit. It does not mean the lender has already won.

In New York, a homeowner usually has a short deadline to respond. If you were personally served in New York, the time to answer may be as little as 20 days. If served by another method, it may be 30 days. The specific deadline depends on the facts, so it is important to have the papers reviewed promptly.

If a homeowner does not answer, the lender may seek a default judgment. A default can make the case much harder to defend because the homeowner may lose the opportunity to raise certain defenses unless the court later permits it.

A foreclosure attorney can prepare and file an answer that may include defenses and counterclaims where appropriate. These may involve issues such as improper service, failure to comply with pre-foreclosure notice requirements, lack of standing, incorrect amounts claimed, statute of limitations concerns, prior foreclosure history, payment disputes, or mortgage servicing errors.

“Standing” is a legal term that generally asks whether the party suing had the right to enforce the note and mortgage when the case was filed. In plain English, the bank or lender must be the proper party to bring the lawsuit. If the paperwork does not support that, it may matter.

During the Settlement Conference Process

Many owner-occupied residential foreclosure cases in New York are eligible for settlement conferences under CPLR 3408. These conferences are court-supervised meetings intended to see whether the case can be resolved, often through a loan modification, repayment plan, short sale, deed in lieu, or other loss mitigation option.

For homeowners, settlement conferences can be both helpful and frustrating. The lender may request repeated financial documents, ask for updated pay stubs or bank statements, deny an application, or claim documents were not received. A lawyer can help organize submissions, track deadlines, identify inconsistent servicer behavior, and advocate for good faith participation.

The New York Department of Financial Services also provides resources for homeowners facing foreclosure and mortgage issues through its help for homeowners materials. These resources can be useful, but they do not replace legal advice when a lawsuit is pending.

A foreclosure attorney may help during settlement conferences by explaining what the court expects, preparing a complete financial package, responding to lender objections, negotiating realistic terms, and making sure the homeowner understands the risks of each proposal. Sometimes the best strategy is to keep pursuing a modification. In other cases, a short sale, bankruptcy, or litigation defense may need to be considered.

When a Loan Modification Has Been Denied or Delayed

A loan modification denial can feel final, but it is not always the end of the road. Denials may be based on missing documents, income calculations, investor restrictions, alleged excessive debt, or servicer mistakes. Sometimes a homeowner may be eligible to appeal the denial or submit a new application if circumstances have changed.

A lawyer can review the denial letter, compare it with the homeowner’s financial documents, and look for errors. For example, a servicer may have misread income, failed to count household contributions, used outdated figures, or failed to explain the denial clearly.

The Consumer Financial Protection Bureau offers consumer information about mortgages and servicing, including loss mitigation concerns. In a pending New York foreclosure case, however, a homeowner may need counsel who can raise servicing problems in court while also negotiating with the lender.

This is especially important if a sale date is approaching. Submitting a modification application does not automatically stop every foreclosure event in every situation. Timing, completeness of the application, court orders, and prior applications can all affect what happens next.

When the Lender Moves for Judgment

If a foreclosure case does not resolve early, the lender may file a motion asking the court for summary judgment, an order of reference, or a judgment of foreclosure and sale. These papers can be intimidating, but they should not be ignored.

A motion for summary judgment is the lender’s request for the court to rule in its favor without a trial. The lender must submit evidence supporting its right to foreclose, the borrower’s default, and the amount due. A homeowner may have grounds to oppose the motion if the lender’s proof is incomplete, inconsistent, or legally defective.

A foreclosure attorney can review the affidavits, business records, assignments, note endorsements, payment history, and claimed arrears. In some cases, the issue is not whether money is owed, but whether the lender has proven the correct amount or complied with the required procedure.

This stage can also be important for preserving appellate rights. If the court grants judgment and there are legal errors, an attorney can evaluate whether an appeal or motion to reargue, renew, or vacate may be appropriate. CGW has handled foreclosure appeals and understands that a careful review of the record can sometimes uncover issues missed earlier in the case.

When a Foreclosure Auction Has Been Scheduled

A scheduled foreclosure auction is urgent. At this stage, waiting can sharply reduce available options. Still, a sale date does not always mean the homeowner must immediately give up.

Depending on the facts, a lawyer may evaluate whether there are grounds to ask the court to stay the sale, whether the judgment or sale notice has defects, whether bankruptcy may be appropriate, whether reinstatement or payoff is possible, whether a short sale can be completed, or whether a last-minute loss mitigation issue needs court attention.

Bankruptcy is one tool that may stop or pause foreclosure through the automatic stay, but it must be used carefully. Chapter 13 may allow some homeowners to catch up on mortgage arrears through a repayment plan while maintaining ongoing mortgage payments. Chapter 7 may help with unsecured debt and provide temporary protection, but it is not usually a long-term cure for mortgage arrears by itself.

For a deeper discussion of timing and sale issues, see CGW’s guide to a New York foreclosure auction sale and how Chapter 13 bankruptcy can help stop foreclosure. Because bankruptcy affects property rights, debt obligations, credit, and court proceedings, homeowners should obtain individualized advice before filing.

When Bankruptcy May Be Part of a Home-Saving Strategy

Bankruptcy should not be viewed as a personal failure. It is a legal tool designed to help people and businesses address debt under court protection. For homeowners facing foreclosure, bankruptcy can sometimes provide breathing room and a structured path forward.

Chapter 13 is often the most relevant option for homeowners who have income but need time to catch up on mortgage arrears. A Chapter 13 plan may allow arrears to be paid over three to five years, while the homeowner continues making current mortgage payments. This can be useful when the main problem is missed payments from a temporary hardship, such as job loss, illness, divorce, or a period of reduced income.

Chapter 7 may help eliminate qualifying unsecured debt, such as credit cards or medical bills, which can free up income. However, if the homeowner is significantly behind on the mortgage and wants to keep the home, Chapter 7 alone may not solve the arrears problem.

Chapter 11 may be relevant for certain small business owners or more complex debt situations, but it is more involved and not the right fit for every case.

Foreclosure defense and bankruptcy strategy should be coordinated. Filing too early, too late, or under the wrong chapter can create problems. CGW’s article on when foreclosure and bankruptcy overlap for New York homeowners explains how these tools can interact.

Signs That a Foreclosure Case Deserves Legal Review

Nearly every foreclosure case benefits from at least an initial legal review, but some warning signs make that review especially important. These include receiving foreclosure papers after years of silence, a loan that was transferred multiple times, a prior foreclosure case that was dismissed, confusion over who owns the loan, payment records that do not match your records, or a denial of a modification despite submitting documents.

Other issues may involve a deceased borrower, divorce, inherited property, a reverse mortgage, a second mortgage, a co-op or condo, tax liens, judgments, or a pending sale contract. These facts can affect strategy and timing.

Homeowners should also be cautious about foreclosure rescue scams. Be wary of anyone who guarantees a modification, asks you to sign over title, tells you to stop communicating with the court, or promises results without reviewing your documents. A legitimate legal strategy should be based on the actual facts of your case.

What to Bring When You Speak With a Foreclosure Attorney

You do not need to have everything perfectly organized before asking for help. Still, bringing key documents can make the first conversation more productive.

Helpful documents may include:

- The summons, complaint, and any court papers you received

- The 90-day notice and other letters from the lender or servicer

- Recent mortgage statements and payment history

- Loan modification applications, denial letters, and servicer correspondence

- Proof of income, tax returns, bank statements, and household expenses

- Any prior foreclosure, bankruptcy, short sale, or modification documents

- Notices of sale, referee documents, or eviction papers if the case is late-stage

If you cannot find certain documents, tell the attorney what you remember. Missing paperwork is common, especially when homeowners have been dealing with stress for months or years.

How Local Experience Can Matter in Westchester and the Hudson Valley

Foreclosure law is statewide, but local practice can still matter. Courts in Westchester County, Rockland County, Putnam County, Orange County, Dutchess County, the Bronx, and nearby areas may have their own procedures, conference practices, scheduling patterns, and expectations.

A local foreclosure defense attorney who regularly handles New York foreclosure cases can help homeowners understand both the law and the practical realities of the courthouse. That includes knowing how settlement conferences tend to proceed, what documents are commonly requested, how to communicate with opposing counsel, and when a court application may be necessary.

For homeowners trying to protect a primary residence, this combination of legal knowledge and local experience can be important. The goal is not simply to delay the case. The goal is to use the time and legal process productively, whether that means defending the foreclosure, pursuing a modification, filing bankruptcy, negotiating a sale, or planning another responsible exit.

Frequently Asked Questions

Can a foreclosure attorney stop foreclosure in New York? A foreclosure attorney may be able to stop, delay, or defend against foreclosure depending on the facts. Options may include filing an answer, raising defenses, negotiating a loan modification, seeking court relief, coordinating a short sale, or using bankruptcy where appropriate. No attorney can guarantee that a foreclosure will be stopped.

Is it too late to get help if I already received a sale date? Not necessarily, but you should act immediately. Once a foreclosure auction is scheduled, time is limited. A lawyer can review whether a stay, bankruptcy filing, reinstatement, payoff, short sale, or other emergency option may be available.

What if I ignored the foreclosure papers and defaulted? A default makes the case harder, but it may still be worth reviewing. Depending on the circumstances, an attorney may evaluate whether there are grounds to vacate the default, challenge service, address notice issues, or pursue another solution.

Do I have to file bankruptcy to save my home? Not always. Some homeowners may pursue foreclosure defenses, loan modifications, repayment arrangements, reinstatement, or short sales without bankruptcy. Bankruptcy may be helpful in certain cases, especially where the homeowner needs time to cure arrears or stop collection activity.

What is the difference between foreclosure defense and loan modification help? Foreclosure defense focuses on the court case and the lender’s legal right to foreclose. Loan modification help focuses on changing the mortgage terms to make payments more affordable. In many New York cases, both strategies may need to be considered together.

Should I keep communicating with my mortgage servicer after hiring an attorney? You should discuss this with your attorney. In many cases, communications should be coordinated so that deadlines are not missed and the servicer receives consistent, complete information.

Speak With a New York Foreclosure Attorney Before Deadlines Pass

If you are behind on your mortgage, received a 90-day notice, were served with a foreclosure summons, or are facing a scheduled auction, you may have more options than you realize. The sooner you get advice, the easier it may be to protect your rights and make informed decisions.

Clair Gjertsen & Weathers PLLC helps homeowners throughout Westchester County, Rockland County, Putnam County, Orange County, Dutchess County, Bronx County, and the Lower Hudson Valley with foreclosure defense, loan modifications, bankruptcy, loss mitigation, short sales, and related litigation.

Every case is unique, and this article is general information rather than legal advice. If your home is at risk, consider contacting CGW to discuss your situation before the next deadline or court date passes.

If you are overwhelmed by credit cards, medical bills, personal loans, or collection notices, it is natural to look for a way to combine everything into one manageable payment. Many New Yorkers search for debt consolidation attorneys because they want relief, but they also want to avoid bankruptcy if possible.

That is understandable. Bankruptcy can feel intimidating, and debt consolidation can sound simpler. But the two options do very different things. Debt consolidation is usually a private repayment or settlement strategy. Bankruptcy is a legal process that may stop collections, discharge qualifying debt, and, in some cases, help homeowners deal with mortgage arrears.

The right choice depends on your income, assets, debt types, whether you have been sued, and whether your home is at risk. This article explains the difference in plain English so you can make a more informed decision before deadlines pass.

Debt consolidation attorneys vs bankruptcy: what is the real difference?

A debt consolidation attorney is not usually providing a loan. Instead, an attorney may help evaluate whether consolidation, settlement, debt defense, or bankruptcy makes sense for your circumstances. The attorney may review creditor claims, negotiate settlements, analyze lawsuits, and help you avoid agreements that create more problems than they solve.

Bankruptcy, by contrast, is a court-supervised legal process. When filed properly, bankruptcy can trigger the automatic stay, which generally pauses most collection activity, including many lawsuits, wage garnishments, bank restraints, and foreclosure steps. Bankruptcy may also eliminate qualifying unsecured debts or reorganize debts through a repayment plan.

In other words, the practical question is not simply attorney versus bankruptcy. The real question is whether an out-of-court debt strategy is enough, or whether you need the stronger protections of bankruptcy law.

What debt consolidation usually means

Debt consolidation is often used as a broad term, but it can mean several different things. Some options are legitimate and helpful in the right situation. Others can be risky, especially when a person is already behind or facing legal action.

Common forms of debt consolidation include:

- A personal loan used to pay off multiple debts

- A balance transfer credit card

- A debt management plan through a nonprofit credit counseling agency

- Negotiated settlements with creditors or collectors

- Refinancing or using home equity to pay unsecured debt

These options may reduce the number of monthly payments or lower interest rates. They may also make budgeting easier. But consolidation does not automatically stop lawsuits, erase judgments, prevent wage garnishment, or stop foreclosure.

Debt settlement also deserves special caution. The Consumer Financial Protection Bureau warns that debt settlement companies often ask consumers to stop paying creditors while money builds in a settlement account. During that time, creditors may still sue, interest and fees may continue, and there is no guarantee a creditor will accept a settlement.

A debt consolidation attorney can help you understand whether the proposal in front of you is realistic, legally sound, and safer than alternatives.

What bankruptcy can do that consolidation cannot

Bankruptcy is not a sign of personal failure. It is a legal tool designed to give honest debtors a structured way to address financial hardship. For some New Yorkers, especially those facing lawsuits, garnishments, foreclosure, or debts that cannot realistically be repaid, bankruptcy may provide protections that consolidation cannot.

The most immediate protection is often the automatic stay. Under federal bankruptcy law, the automatic stay generally stops most collection activity after a bankruptcy petition is filed. The U.S. Courts bankruptcy basics guide explains the general structure of bankruptcy relief, including the different chapters available to individuals and businesses.

For individuals and homeowners in New York, the most common bankruptcy chapters are Chapter 7 and Chapter 13.

| Bankruptcy chapter | Basic purpose | Common use |

|---|---|---|

| Chapter 7 | Liquidation bankruptcy that may eliminate qualifying unsecured debt | Credit cards, medical bills, personal loans, and other dischargeable unsecured debts when the debtor qualifies |

| Chapter 13 | Reorganization bankruptcy with a 3-to-5-year repayment plan | Catching up on mortgage arrears, stopping foreclosure, protecting assets, and repaying debts over time |

| Chapter 11 | Reorganization often used by businesses or individuals with complex debt | Business restructuring, larger debt situations, and continued operations where appropriate |

For a deeper overview of bankruptcy basics, CGW has also published Consumer Bankruptcy 101, which explains Chapter 7, Chapter 13, exemptions, and discharge issues in more detail.

Key differences for New York consumers

Debt consolidation and bankruptcy can both affect your financial future, but they work in very different ways. The table below gives a practical comparison.

| Issue | Debt consolidation or settlement | Bankruptcy |

|---|---|---|

| Creditor participation | Usually requires creditor agreement or a new lender willing to extend credit | Creditors are generally bound by bankruptcy law once the case is filed |

| Lawsuits | May not stop a pending lawsuit unless the creditor agrees or the case is defended | The automatic stay may pause many lawsuits and collection actions |

| Wage garnishment or bank restraint | May continue unless resolved separately | The automatic stay may stop many garnishments and restraints, depending on the facts |

| Credit card and medical debt | May be repaid, refinanced, or settled | May be discharged if the debt qualifies |

| Mortgage arrears | Usually not enough by itself to cure serious arrears | Chapter 13 may allow arrears to be repaid over time while ongoing mortgage payments continue |

| Home risk | Using home equity to consolidate unsecured debt can put the home at greater risk | Exemptions and Chapter 13 planning may help protect a home, depending on equity and income |

| Tax issues | Forgiven debt may create tax consequences in some cases | Discharged debt in bankruptcy is generally treated differently for tax purposes, but tax advice may still be needed |

| Public record | Usually private unless litigation or judgments are involved | Bankruptcy filings are public court records |

No option is automatically better for everyone. A manageable consolidation plan can be appropriate for someone with steady income and no active lawsuits. Bankruptcy may be more appropriate when creditors are already taking legal action or when debt has become impossible to repay within a realistic budget.

When debt consolidation may make sense

Debt consolidation may be worth considering when your financial distress is serious but still manageable. This often means you have steady income, your essential expenses are under control, and you are not already facing multiple lawsuits or enforcement actions.

For example, consolidation may help if most of your debt is high-interest credit card debt, you qualify for a lower-interest loan, and the new payment truly fits your monthly budget. A nonprofit debt management plan may also help some consumers reduce interest rates and pay debts in a structured way.

An attorney can be especially helpful when collection accounts are involved. Before paying or settling older debt, it may be important to know whether the creditor can still sue you. New York’s Consumer Credit Fairness Act shortened the statute of limitations for many consumer credit transactions and added important protections for debtors. CGW discusses those changes in How the New York Consumer Credit Fairness Act Benefits Debtors.

Debt consolidation may be a better fit when:

- You can afford the proposed payment without falling behind on rent, mortgage, utilities, food, insurance, or taxes

- You are not using your home as collateral for unsecured credit card or medical debt

- You have not been served with multiple lawsuits or enforcement notices

- The creditor or collector will provide a clear written settlement agreement

- The total repayment amount is realistic compared with your income

- You understand any tax, credit, or legal consequences before agreeing

The key word is realistic. A consolidation plan that only works on paper may delay the problem while interest, late fees, lawsuits, or foreclosure pressure continue to build.

When bankruptcy may be the better tool

Bankruptcy may be worth discussing when debt has moved beyond ordinary budgeting problems. If you are being sued, facing wage garnishment, dealing with a frozen bank account, or receiving foreclosure papers, you may need legal protection rather than another payment arrangement.

Chapter 7 may help people who have limited income and mostly unsecured debts, such as credit cards, medical bills, or personal loans. It can provide a fresh start if the person qualifies and if assets are protected by exemptions.

Chapter 13 may be more useful for homeowners who need time to catch up on mortgage arrears. In a Chapter 13 case, a homeowner may be able to propose a plan to repay arrears over time while staying current on ongoing mortgage payments. This can be especially important when foreclosure has already started.

CGW has written more about the differences between the two chapters in Chapter 7 vs Chapter 13 Bankruptcy in Westchester and the Hudson Valley.

Bankruptcy may deserve serious consideration if:

- Your debt payments are greater than your realistic monthly surplus

- You have been served with a creditor lawsuit

- A judgment, wage garnishment, or bank restraint is already in place

- You are behind on your mortgage and foreclosure is pending or likely

- You need a court-supervised way to address debt rather than voluntary creditor cooperation

- You have tried consolidation before and the debt has continued to grow

For many residents of Westchester, Rockland, Putnam, Orange, Dutchess, and Bronx County, bankruptcy cases are generally handled in the U.S. Bankruptcy Court for the Southern District of New York. Local procedure, trustee expectations, exemptions, and foreclosure timing can all matter.

A special warning for New York homeowners

If you own a home, be especially careful before using home equity to consolidate unsecured debt. Credit card debt and medical debt are usually unsecured, meaning the creditor does not automatically have a mortgage on your home. But if you refinance, take a home equity loan, or use another secured product to pay those debts, you may be converting unsecured debt into debt secured by your home.

That can be dangerous. If the new payment becomes unaffordable, you may have placed your home at risk for debts that might otherwise have been negotiated, defended, or discharged in bankruptcy.

This issue is especially important for homeowners in Westchester County, Rockland County, Putnam County, Orange County, Dutchess County, the Bronx, and the Lower Hudson Valley, where home values and living costs can be high. Home equity can be an important asset, but it should be evaluated carefully before it is used to pay old unsecured debt.

If mortgage arrears are already part of the problem, consolidation alone may not be enough. Other options may include foreclosure defense, a loan modification, bankruptcy, short sale planning, or a combination of strategies. CGW explains how foreclosure and bankruptcy can overlap in When Foreclosure and Bankruptcy Overlap for New York Homeowners.

What if you have already been sued by a creditor?

If you have been served with a summons and complaint, do not ignore it. A debt consolidation plan does not automatically answer the lawsuit for you. If you miss the deadline to respond, the creditor may seek a default judgment.

Once a judgment is entered, the creditor may have additional collection tools, including wage garnishment, bank restraints, and liens in certain circumstances. New York law provides important debtor protections, but those protections usually work best when raised properly and on time.

A lawyer can review whether the creditor has the documents needed to prove the debt, whether the statute of limitations has expired, whether the lawsuit was served properly, and whether settlement or bankruptcy should be considered. CGW discusses these issues further in Debt Lawsuits and Your Home: When a New York Bankruptcy Attorney Can Help.

The most important step is to act before a default judgment or enforcement action makes the problem harder to fix.

How to decide between consolidation and bankruptcy

There is no one-size-fits-all answer. The best option depends on your full financial picture, not just the amount you owe.

| Question to ask | Why it matters |

|---|---|

| Are you current on your mortgage or rent? | Housing stability should usually come before unsecured debt repayment |

| Have you been sued or garnished? | Active legal action may require immediate legal response |

| Can you afford a consolidation payment for the full term? | A payment that is too high can lead to default and more debt |

| Are you using home equity to pay unsecured debt? | This may increase the risk to your home |

| Do you qualify for Chapter 7 or Chapter 13? | Eligibility affects whether bankruptcy is practical |

| Do you have tax debt, student loans, support obligations, or recent debts? | Some debts are treated differently and may not be discharged easily |

| Is foreclosure pending? | Timing can be critical, especially if a sale date is approaching |

A useful way to think about the decision is this: consolidation works best when creditors are cooperative and your budget can support repayment. Bankruptcy may be more appropriate when you need legal protection, a discharge, or a structured court process to deal with debt and protect essential assets.

Documents to gather before speaking with an attorney

Whether you are considering debt consolidation, bankruptcy, or both, good information helps an attorney give meaningful guidance. Try to gather:

- Recent pay stubs or proof of income

- Bank statements

- Credit card and collection statements

- Lawsuit papers, judgments, garnishment notices, or bank restraint notices

- Mortgage statements, foreclosure papers, or loan modification correspondence

- Tax returns

- A list of monthly household expenses

- Any settlement offers or debt consolidation proposals you have received

Do not worry if you do not have everything. If you are under pressure from a lawsuit, foreclosure, or garnishment, it is often better to ask for help quickly and supplement documents later.

Why timing matters

Waiting rarely improves a serious debt problem. Interest may continue. Lawsuit deadlines may pass. Judgments may be entered. Foreclosure cases may move toward settlement conferences, motion practice, judgment of foreclosure and sale, or auction.

Early legal advice can preserve options. A consumer who acts before judgment may have defenses or settlement leverage. A homeowner who acts before a foreclosure sale may have more time to evaluate bankruptcy, loan modification, or other home-saving strategies. A person considering bankruptcy may be able to avoid mistakes, such as transferring property, draining retirement funds, or taking on risky secured debt.

You do not need to know the perfect solution before speaking with an attorney. The purpose of the consultation is to understand the options and risks before choosing a path.

Frequently Asked Questions

Can a debt consolidation attorney stop a creditor lawsuit in New York? An attorney may be able to defend the lawsuit, negotiate a settlement, or evaluate bankruptcy options, but consolidation by itself does not automatically stop a lawsuit. If you have been served, you should act quickly because court deadlines may apply.

Is bankruptcy better than debt consolidation? Not always. Debt consolidation may work when the debt is manageable and creditors cooperate. Bankruptcy may be better when you need legal protection, are facing lawsuits or garnishment, or cannot realistically repay the debt. Every case depends on the facts.

Will bankruptcy stop foreclosure in New York? Bankruptcy may temporarily stop many foreclosure actions through the automatic stay. Chapter 13 may also allow some homeowners to repay mortgage arrears over time, depending on income, equity, and the feasibility of the plan. It is important to seek advice before a foreclosure sale date.

Can I consolidate debt after being sued? Possibly, but a lawsuit creates added urgency. You may still need to answer the complaint or address the case in court. A settlement should be in writing and should clearly state what happens to the lawsuit, judgment, and any collection activity.

Does debt consolidation hurt credit less than bankruptcy? It depends. Missed payments, settlements, charged-off accounts, judgments, and bankruptcy can all affect credit. A consolidation plan that fails may cause more long-term harm than a carefully planned legal solution. Credit impact should be considered, but it should not be the only factor.

Should I use a home equity loan to pay credit cards? Be cautious. Using home equity to pay unsecured credit card debt can put your home at risk if you later cannot make the new payments. Homeowners should speak with qualified counsel before converting unsecured debt into debt secured by a home.

Speak with a New York debt and bankruptcy attorney before options narrow

If you are comparing debt consolidation attorneys vs bankruptcy in New York, you are already taking an important step. The next step is to understand which option fits your actual situation, including your income, assets, lawsuits, mortgage status, and long-term goals.

Clair Gjertsen & Weathers PLLC helps New Yorkers facing debt lawsuits, creditor pressure, bankruptcy questions, foreclosure, and mortgage-related hardship. The firm works with clients throughout Westchester County, Rockland County, Putnam County, Orange County, Dutchess County, Bronx County, and the Lower Hudson Valley.

If you are unsure whether consolidation, bankruptcy, foreclosure defense, or another strategy is right for you, consider speaking with experienced legal counsel before deadlines pass. Early action may create more options and reduce the risk of avoidable financial harm.

If you are behind on mortgage payments or have already received foreclosure papers, it is easy to feel as if the process is moving faster than you can understand it. In New York, however, foreclosure is a legal process with stages, notices, deadlines, defenses, and opportunities to negotiate.

That does not mean every homeowner can keep the home in every case. It does mean that waiting, ignoring papers, or relying only on conversations with the mortgage servicer can reduce your options. Experienced foreclosure lawyers can help you understand where you are in the process, what deadlines matter, and which legal or financial strategies may be available.

Below is a practical stage-by-stage guide to what foreclosure lawyers can do in New York, from the first missed payments through settlement conferences, litigation, auction, appeal, and post-sale issues.

Why the stage of foreclosure matters in New York

New York is a judicial foreclosure state. In most residential mortgage cases, a lender cannot simply take your home without going through court. The lender must file a lawsuit, serve legal papers, and ultimately obtain a judgment before a foreclosure sale can occur.

The New York State Unified Court System explains foreclosure as a court process, and that court process creates opportunities for homeowners to respond. But those opportunities are tied to deadlines. A homeowner who acts after receiving a 90-day notice may have more options than someone who waits until the morning of an auction.

A lawyer’s role also changes over time. Early on, the focus may be loss mitigation, loan modification, and document review. After a lawsuit begins, the focus may shift to filing an answer, asserting defenses, attending settlement conferences, opposing motions, or considering bankruptcy. Near a sale date, the strategy may become more urgent and time-sensitive.

Quick overview: what foreclosure lawyers may do at each stage

| Stage of foreclosure | What may be happening | How a foreclosure lawyer may help |

|---|---|---|

| Missed payments | The servicer sends default letters, calls, or repayment demands | Review the loan, assess the arrears, explain options, and help communicate with the servicer |

| 90-day pre-foreclosure notice | The lender may be preparing to sue | Review whether required notices were sent properly and help pursue loss mitigation |

| Summons and complaint | A foreclosure lawsuit has started | File an answer, preserve defenses, and prevent a default where possible |

| Settlement conference | The court schedules conferences for eligible residential cases | Prepare financial documents, negotiate, and address servicer delays or errors |

| Active litigation | The lender seeks summary judgment or a referee computes the debt | Challenge legal defects, oppose motions, request discovery, and review the amount claimed |

| Judgment of foreclosure and sale | The court authorizes a sale | Evaluate objections, appeals, bankruptcy, reinstatement, sale, or modification options |

| Auction scheduled | A sale date is approaching | Consider emergency applications, bankruptcy, payoff, short sale, or other urgent strategies |

| After auction | Ownership and possession issues may arise | Review sale issues, surplus funds, deficiency risk, eviction timing, and possible appeals |

| Appeal stage | A homeowner challenges an adverse order or judgment | Identify legal errors, seek stays where appropriate, and pursue appellate relief |

Stage 1: Behind on mortgage payments but no lawsuit yet

Many homeowners wait to call a lawyer because they have not yet been sued. In reality, this can be one of the most important times to get legal advice.

At this stage, a foreclosure lawyer may review the mortgage, payment history, escrow charges, servicer letters, and hardship circumstances. The goal is to understand whether the arrears are accurate, whether the servicer has made mistakes, and whether there is a realistic path to catching up or modifying the loan.

Common early-stage options may include repayment plans, forbearance review, reinstatement, loan modification, refinance, sale, or short sale. Which option makes sense depends on income, equity, arrears, hardship, family goals, and how much time is available.

For homeowners trying to keep the home, a loan modification may be worth exploring. A modification can potentially change the loan terms, such as the monthly payment, interest rate, term, or treatment of arrears, depending on the lender’s programs and the borrower’s circumstances. You can learn more about this option in CGW’s guide on how to apply for a loan modification.

A lawyer can also help you avoid dangerous mistakes, such as submitting incomplete modification packages, missing servicer deadlines, ignoring written notices, or relying on promises that are not confirmed in writing.

Stage 2: After receiving a 90-day pre-foreclosure notice

In many New York residential mortgage cases, a lender must send a 90-day pre-foreclosure notice before filing the lawsuit. This notice is often referred to as an RPAPL 1304 notice.

The notice is not the same as a lawsuit. It is a warning that the lender may start foreclosure if the default is not resolved. For many homeowners, it is also a critical opportunity to act before court papers arrive.

Foreclosure lawyers may help by reviewing whether the notice appears to comply with New York requirements, whether it was sent to the proper borrower or borrowers, and whether the timing of the lawsuit is proper. Notice defects can sometimes become important defenses later, depending on the facts.

A lawyer may also use this period to help organize a loss mitigation application, communicate with the servicer, review financial documents, and create a plan before litigation begins. For a deeper discussion of this notice, see CGW’s article on the RPAPL 1304 90-day pre-foreclosure notice.

Stage 3: After being served with a summons and complaint

Once you are served with a summons and complaint, the foreclosure case has officially begun. This is not the time to ignore the papers or assume that a loan modification application will automatically protect you.

In New York, the deadline to answer a foreclosure complaint is often 20 or 30 days, depending on how service was made and other procedural factors. If you do not respond, the lender may seek a default judgment. A default can make it much harder to raise defenses later.

At this stage, foreclosure lawyers may:

- Review how and when you were served

- File an answer on your behalf

- Assert affirmative defenses where supported by the facts

- Review whether the lender has standing to sue

- Examine compliance with pre-foreclosure notice requirements

- Identify payment, escrow, or accounting disputes

- Protect your ability to participate meaningfully in the case

An answer is not just a formality. It is often the document that preserves your legal defenses. Even if you are also seeking a modification, filing a proper legal response can be essential.

Stage 4: Settlement conferences in residential foreclosure cases

For many owner-occupied residential foreclosure cases in New York, the court schedules mandatory settlement conferences. These conferences are designed to explore whether the case can be resolved without a foreclosure sale, often through a loan modification or other loss mitigation option.

Settlement conferences can be confusing for homeowners. Servicers may request repeated documents, claim items are missing, or deny a modification for reasons that are difficult to understand. A lawyer can help you prepare a complete package, track submissions, respond to requests, and raise issues with the court when the process is not moving fairly.

A foreclosure lawyer may also help explain whether a proposed modification is affordable and sustainable. A payment that looks manageable for one month may not be workable long term if it ignores taxes, insurance, household expenses, or other debt.

In settlement conferences, the lawyer’s role is not only to negotiate. It is also to create a clear record of what was submitted, what the servicer requested, and whether the parties are participating in good faith.

Stage 5: Active foreclosure litigation

If the case does not resolve in settlement conferences, it may proceed into litigation. This is where legal defenses become especially important.

Foreclosure litigation can involve discovery, motion practice, summary judgment, referee proceedings, and challenges to the amount allegedly owed. The lender may ask the court to rule in its favor without a trial. The homeowner may have the right to oppose that request if there are valid factual or legal grounds.

Common issues foreclosure lawyers evaluate include:

| Legal issue | Why it may matter |

|---|---|

| Standing | The lender must generally show it had the right to enforce the note and mortgage when the case began |

| Notice compliance | Required pre-foreclosure notices must be sent correctly in many residential cases |

| Statute of limitations | Some foreclosure claims may be time-barred if too much time has passed after acceleration |

| Payment history | Errors in credits, fees, escrow, or arrears can affect the amount claimed |

| Service of process | Defective service may affect the court’s personal jurisdiction over a borrower |

| Referee calculations | The amount due must be supported by proper proof and accounting |

Not every case has strong defenses. But homeowners should not assume the bank’s paperwork is automatically correct. A careful legal review can make a significant difference in how the case is handled, whether through litigation, negotiation, or another strategy.

Stage 6: Judgment of foreclosure and sale

A judgment of foreclosure and sale is a serious point in the case. It generally means the court has authorized the property to be sold at auction, subject to the procedures required in the judgment and applicable law.

Even at this stage, a lawyer may still have work to do. The lawyer may review whether the judgment was properly entered, whether the amount owed was accurately calculated, whether there are grounds to object, and whether any appeal or motion practice is appropriate.

This is also a stage where strategy becomes highly fact-specific. Some homeowners may still be trying to keep the home. Others may be considering a sale, short sale, deed in lieu, bankruptcy, or negotiated move-out timeline. A lawyer can help compare options and avoid decisions that create unnecessary financial exposure.

If a sale date has not yet been scheduled, there may be more time to evaluate alternatives. If a sale date is already scheduled, urgent action may be required.

Stage 7: When a foreclosure auction is scheduled

A scheduled foreclosure auction does not always mean there is nothing left to do. It does mean the situation is urgent.

At this stage, foreclosure lawyers may evaluate whether there is a legal basis to ask the court to stop or postpone the sale. This could involve an emergency motion, a challenge to notice or procedure, a pending modification issue, a bankruptcy filing, or another case-specific argument. Whether any of these options is available depends on the facts and timing.

Bankruptcy may be particularly relevant for some homeowners. When a bankruptcy case is filed, the automatic stay may temporarily stop foreclosure activity, including a scheduled sale. Chapter 13 bankruptcy may allow a qualifying homeowner to repay mortgage arrears over time while staying current on ongoing payments. Chapter 7 may provide temporary protection from collection activity, but it is usually not designed as a long-term mortgage arrears repayment tool.

Bankruptcy is not appropriate for everyone. It must be filed carefully and honestly, with attention to income, assets, debts, prior filings, and long-term goals. Repeat filings or filings made in bad faith can limit protection. CGW discusses these issues further in its article on when foreclosure and bankruptcy overlap for New York homeowners.

For more on the auction process itself, see CGW’s overview of a New York foreclosure auction sale.

Stage 8: After the foreclosure sale

After a foreclosure auction, options become more limited, but homeowners may still have rights that should be reviewed.

A lawyer may examine whether the sale was properly noticed and conducted, whether there are grounds to challenge the sale, and what happens next regarding possession. If the homeowner or occupants remain in the property, a post-foreclosure eviction or possession proceeding may follow.

There may also be financial issues after sale. If the property sells for more than the debt and related costs, surplus funds may exist. If the property sells for less than the amount owed, the lender may consider seeking a deficiency judgment, subject to New York rules and deadlines. These issues are separate from the emotional impact of losing a home, but they can significantly affect a family’s financial recovery.

Homeowners should not ignore post-sale paperwork. A lawyer can help determine whether there is a surplus claim, whether a deficiency issue exists, whether bankruptcy should be considered for remaining debt, and whether more time in the property can be negotiated or lawfully obtained. CGW also has a detailed article on post-foreclosure eviction options in New York.

Stage 9: Foreclosure appeals

Appeals are different from trial-level foreclosure defense. An appeal asks a higher court to review whether legal errors occurred in the lower court.

A foreclosure lawyer handling appeals may review orders granting summary judgment, orders confirming a referee’s report, judgments of foreclosure and sale, and other decisions that affected the homeowner’s rights. The lawyer may also evaluate whether to seek a stay pending appeal, because filing an appeal by itself does not always stop a sale or enforcement activity.

Appeal deadlines can be short and technical. If you believe the court made a mistake, or if you received an order you do not understand, it is important to seek legal guidance quickly. Waiting can affect whether appellate rights are preserved.

How foreclosure lawyers connect legal defense with practical goals

A strong foreclosure strategy is not always about one single tactic. It is often about matching the legal tools to the homeowner’s real goal.

| Homeowner goal | Possible legal or practical tools |

|---|---|

| Keep the home | Loan modification, Chapter 13 bankruptcy, settlement conferences, reinstatement, litigation defenses |

| Get time to transition | Negotiated timelines, court applications, short sale, bankruptcy where appropriate |

| Challenge lender errors | Foreclosure defense, discovery, motion opposition, accounting review, appeal |

| Reduce overall debt pressure | Chapter 7, Chapter 13, debt defense, settlement, budgeting and financial review |

| Sell the home before auction | Traditional sale, short sale, payoff coordination, motion practice if time is needed |

| Address post-sale issues | Surplus funds review, deficiency defense, occupancy negotiation, eviction defense |

This is why personalized representation matters. Two homeowners may both be six months behind, but their best options may be completely different depending on income, equity, family needs, loan history, prior court activity, and debt load.

Documents to gather before speaking with a foreclosure lawyer

You do not need to have everything perfectly organized before calling a lawyer. But if you can gather key documents, the first consultation is usually more productive.

Helpful documents include:

- The summons and complaint, if you were sued

- Any 90-day notice, default letter, or acceleration letter

- Recent mortgage statements and payment history

- Loan modification applications and denial letters

- Correspondence from the servicer, lender, or law firm

- Court orders, conference notices, or sale notices

- Proof of income, bank statements, and monthly expenses

- Property tax, insurance, and escrow information

- Bankruptcy papers from any prior filing

- Documents showing other debts, judgments, or collection lawsuits

If you are missing documents, say so. A lawyer may still be able to review the docket, request information, or help you identify what is needed.

How to choose a foreclosure lawyer in New York

When your home is at risk, it is important to work with counsel who understands both the court process and the practical realities of mortgage servicing.

Consider whether the lawyer or firm has experience with New York foreclosure defense, settlement conferences, loan modification issues, bankruptcy, foreclosure appeals, and post-sale matters. Local knowledge can also matter, especially in Westchester County, Rockland County, Putnam County, Orange County, Dutchess County, Bronx County, and the broader Lower Hudson Valley.

You should also feel that the lawyer is explaining your options clearly. A trustworthy lawyer will not guarantee that you will keep your home, win the case, or receive a modification. Instead, the lawyer should help you understand risks, deadlines, likely next steps, and available strategies based on your specific circumstances.

Frequently Asked Questions

Can foreclosure lawyers stop foreclosure in New York? A foreclosure lawyer may be able to stop, delay, challenge, or resolve a foreclosure depending on the circumstances. Possible tools include foreclosure defense, settlement conferences, loan modification, bankruptcy, appeals, or negotiated alternatives. No lawyer can guarantee a specific outcome.

When should I contact a foreclosure lawyer? You should consider contacting a lawyer as soon as you miss payments, receive a 90-day notice, get served with a summons and complaint, or learn of a sale date. Early action often creates more options.

Do I still need to answer the foreclosure complaint if I am applying for a loan modification? In most cases, yes. A loan modification application does not automatically protect you from defaulting in the court case. A lawyer can help you respond to the lawsuit while also pursuing loss mitigation.

What happens at a New York foreclosure settlement conference? The court conference is an opportunity to explore alternatives to foreclosure, often through a loan modification or other resolution. A lawyer can help prepare documents, communicate with the servicer, and address delays or problems in the process.

Can bankruptcy stop a foreclosure auction? A bankruptcy filing may trigger the automatic stay, which can temporarily stop a foreclosure sale. Whether bankruptcy is appropriate depends on income, assets, debts, prior filings, timing, and long-term goals.

Is it too late to call a lawyer if the auction is already scheduled? Not necessarily, but time is critical. A lawyer may review whether an emergency court application, bankruptcy, reinstatement, payoff, sale, or other strategy is available. The closer the sale date is, the fewer options may remain.

What if the foreclosure sale already happened? You may still need advice about possession, post-foreclosure eviction, surplus funds, deficiency judgment risk, appeal rights, or bankruptcy options for remaining debt. Post-sale deadlines and procedures should be reviewed promptly.

Talk with a New York foreclosure defense lawyer before deadlines pass

Foreclosure is stressful, but you do not have to navigate it alone. Whether you just received a 90-day notice, were served with a lawsuit, are in settlement conferences, or are facing a scheduled auction, legal guidance can help you understand your rights and make informed decisions.

Clair Gjertsen & Weathers PLLC helps homeowners in Westchester County, the Lower Hudson Valley, Bronx County, and surrounding New York communities evaluate foreclosure defense, loan modification, bankruptcy, appeals, short sales, and post-foreclosure options.

If your home is at risk, consider reaching out before the next deadline passes. Contact Clair Gjertsen & Weathers PLLC to discuss your situation and the options that may be available based on your circumstances.

If you are behind on your mortgage or have been served with foreclosure papers, it can feel like the bank has all the power. In New York, that is not the case. Foreclosure is a court process, and homeowners have rights at each stage of that process.

Foreclosure defense lawyers protect homeowners by forcing the lender to prove its case, identifying legal defenses, helping pursue loss mitigation, responding to motions, and building a strategy that fits the homeowner's real goals. For some families, the goal is to keep the home. For others, it may be more time, a better transition, a short sale, or protection from a larger financial crisis.

The most important point is this: waiting usually reduces your options. A lawyer can often do more before a judgment or auction than after one, although options may still exist even late in the case.

Foreclosure Defense in New York Starts With Understanding the Process

New York is a judicial foreclosure state. That means a mortgage lender generally must file a lawsuit and obtain a court judgment before it can sell a home at a foreclosure auction. The lender cannot simply change the locks because a borrower missed payments.

According to the New York State Unified Court System, homeowners who receive foreclosure papers should not ignore them. A foreclosure lawsuit has deadlines, and missing those deadlines can make the case harder to defend.

A foreclosure defense lawyer helps the homeowner understand where the case stands, what deadlines apply, and which legal or financial options may still be available. This is especially important in Westchester County, Rockland County, Putnam County, Orange County, Dutchess County, the Bronx, and throughout the Lower Hudson Valley, where foreclosure cases move through the New York Supreme Court system.

What Foreclosure Defense Lawyers Actually Do

A foreclosure defense lawyer does more than file papers to buy time. The lawyer's role is to examine the lender's case, protect the homeowner's procedural rights, and help create a realistic path forward.

In plain English, foreclosure defense may include:

- Reviewing the summons, complaint, mortgage, note, assignments, payment history, and notices

- Determining whether the lender complied with New York pre-foreclosure requirements

- Preparing and filing an answer with defenses and counterclaims when appropriate

- Appearing in court and at settlement conferences

- Challenging unsupported fees, interest, escrow charges, or loan balances

- Negotiating with the lender or servicer for a loan modification or other resolution

- Coordinating foreclosure defense with bankruptcy, short sale, or appeal strategies when needed

Every case is different. A homeowner who missed three payments and has not yet been sued is in a very different position from a homeowner facing a scheduled auction next week. Good foreclosure defense begins with a case-specific review, not a generic promise.

Reviewing Pre-Foreclosure Notices and Lender Compliance

Before a lender starts many residential foreclosure actions in New York, it must comply with strict notice rules. One of the most important is the RPAPL 1304 90-day notice, which gives certain borrowers advance warning before a foreclosure lawsuit is filed.

This notice is not a minor technicality. New York courts have often required strict compliance with the statute. A defect in the notice, mailing, timing, or content may create a defense, depending on the facts.

A lawyer may review whether:

- The notice was sent to each required borrower

- The notice was mailed in the required manner

- The lender waited the required time before suing

- The language of the notice complied with New York law

- The lender made required filings related to the notice

CGW has written more about this issue in its discussion of the RPAPL 1304 90-day pre-foreclosure notice. If you received a 90-day notice, that is often the right time to get legal advice, not the time to wait and hope the problem disappears.

Responding When You Are Served With a Foreclosure Lawsuit

Once a homeowner is served with a summons and complaint, the clock starts running. Depending on how service was made, a homeowner may have a limited time to respond. Failing to answer can lead to a default, which can make it easier for the lender to move toward judgment.

Foreclosure defense lawyers help homeowners file a proper response. That response may deny allegations, raise affirmative defenses, and preserve legal arguments that could otherwise be lost.

Common foreclosure defenses in New York may involve:

- Lack of standing, meaning the plaintiff may not have had the right to sue when the case began

- Defective pre-foreclosure notices

- Statute of limitations problems

- Errors in the amount claimed due

- Failure to comply with mortgage servicing rules

- Improper assignments or missing loan documents

- Predatory lending or other loan origination issues, when supported by the facts

These defenses do not apply in every case. A defense must be supported by evidence and law. But when valid issues exist, raising them early can protect the homeowner and may improve the chances of a more favorable resolution.

Protecting Homeowners at Each Stage of Foreclosure

Foreclosure defense is not one single tactic. The right strategy depends on timing, finances, court history, and the homeowner's goals.

| Stage of foreclosure | How a lawyer may help | Why it matters |

|---|---|---|

| Behind on payments, no lawsuit yet | Review notices, explore forbearance, modification, repayment, or other workout options | Early action may prevent a lawsuit or preserve more choices |

| 90-day notice received | Check compliance and prepare a response strategy | Notice defects may become important later |

| Summons and complaint served | File an answer and preserve defenses | Missing the response deadline can lead to default |

| Settlement conference scheduled | Prepare documents, negotiate, and address servicer delays | Many homeowners seek loan modification review at this stage |

| Lender files motions | Oppose summary judgment or other requests when grounds exist | Motions can move the case toward judgment quickly |

| Judgment or auction scheduled | Consider emergency motions, bankruptcy, payoff, reinstatement, or sale alternatives | Late action may still help, but options are narrower |

| After sale | Review eviction issues, surplus funds, or possible challenges | Some rights may remain even after auction |

This staged approach is important because homeowners often assume it is too early or too late to call a lawyer. In reality, timing changes the strategy, but it does not always eliminate the possibility of legal help.

Using Settlement Conferences and Loan Modification Reviews

In many New York residential foreclosure cases involving an owner-occupied home, the court schedules a settlement conference. The purpose is to see whether the case can be resolved without foreclosure, often through loan modification, repayment, reinstatement, short sale, or another loss mitigation option.

These conferences can be valuable, but they can also be frustrating. Homeowners may submit documents repeatedly, only to be told something is missing. A servicer may change representatives, request updated bank statements, or deny an application for reasons that are difficult to understand.

A foreclosure defense lawyer can help by organizing the financial package, tracking submissions, challenging improper denials, and making a record if the lender or servicer fails to negotiate appropriately. While no attorney can guarantee a modification, legal representation can help reduce avoidable mistakes and keep pressure on the process.

For homeowners trying to keep their property, a loan modification may be one possible solution. The best approach usually depends on income, arrears, property value, loan type, and whether the homeowner can afford future payments.

Challenging the Amount Claimed Due

Foreclosure cases often involve more than missed principal and interest. The lender's claimed balance may include late charges, legal fees, property inspections, escrow advances, insurance charges, interest, and other costs.

A lawyer may review whether the claimed amount is properly supported. This can matter greatly. An inflated payoff figure may make reinstatement, sale, refinancing, or modification more difficult. In some cases, the amount due becomes a central issue before judgment or before a referee computes the debt.

Homeowners should keep mortgage statements, correspondence, proof of payments, modification applications, escrow notices, insurance records, tax records, and any letters from the servicer. Those documents may help a lawyer identify inconsistencies or errors.

Coordinating Foreclosure Defense With Bankruptcy Options

Foreclosure does not always happen in isolation. Many homeowners are also dealing with credit card debt, medical bills, tax issues, car payments, or creditor lawsuits. In those situations, bankruptcy may be part of the larger strategy.

Bankruptcy is not a personal failure. It is a legal tool that may help people reorganize or eliminate certain debts, stop collection activity, and create breathing room. When foreclosure is involved, bankruptcy must be considered carefully and timed properly.

Chapter 13 bankruptcy may help some homeowners stop a foreclosure sale and repay mortgage arrears over time through a court-supervised repayment plan, while also keeping up with ongoing mortgage payments. Chapter 7 may help with unsecured debt, but it usually does not provide the same long-term structure for curing mortgage arrears. Chapter 11 may be relevant for some small business owners or more complex financial situations.

CGW discusses this topic further in its article on how Chapter 13 bankruptcy can help stop foreclosure in New York. Bankruptcy should not be filed casually, especially close to a foreclosure sale. A lawyer can help evaluate whether it fits the homeowner's goals, budget, equity position, and long-term plan.

Responding to a Scheduled Foreclosure Auction

A scheduled auction is serious, but it does not always mean every option is gone. Depending on the circumstances, a lawyer may evaluate whether there are grounds to seek emergency court relief, oppose the sale, pursue bankruptcy protection, negotiate a reinstatement or payoff, request an adjournment, or explore alternatives such as a short sale.

Late-stage foreclosure defense is highly fact-specific. Courts generally want to see a valid legal basis for emergency relief. Filing papers at the last minute without a real strategy can create problems. Still, homeowners should not assume there is nothing to do simply because a sale date has been set.

If you are approaching an auction, review CGW's guide on how to stop foreclosure in Westchester and the Hudson Valley and speak with counsel as soon as possible.

Preserving Appellate Rights When the Court Gets It Wrong

Sometimes a homeowner receives an unfavorable ruling even though there may be legal or factual problems with the decision. In those situations, an appeal or motion for reconsideration may be worth evaluating.

Foreclosure appeals require careful analysis. A lawyer must review the order, judgment, motion papers, evidence, court record, deadlines, and potential legal errors. Not every adverse ruling is appealable, and not every appeal is practical. But when a court has overlooked important issues, misapplied the law, or relied on insufficient proof, appellate review may provide another path.

This is one reason it helps to work with a firm that understands both foreclosure litigation and foreclosure appeals. The earlier appellate issues are identified, the easier it may be to preserve them.

Helping Homeowners Make Practical Decisions

Not every foreclosure case ends with the homeowner keeping the property. Sometimes the best legal strategy is to create time for a sale, negotiate a short sale, resolve deficiency exposure, protect remaining equity, or plan for a controlled move.

A foreclosure defense lawyer should help the homeowner understand realistic options, not simply tell them what they want to hear. That may include discussing:

- Whether the home is affordable going forward

- Whether arrears can be cured through modification, repayment, or Chapter 13

- Whether the property has equity worth protecting

- Whether a sale or short sale may reduce financial harm

- Whether bankruptcy could address other debts

- Whether post-foreclosure eviction issues need to be planned for

This practical guidance can be just as important as courtroom defense. Foreclosure affects housing, credit, family stability, and future financial recovery. The legal strategy should reflect the full picture.

What Foreclosure Defense Lawyers Cannot Guarantee

It is important to be honest about limits. Foreclosure defense lawyers cannot guarantee that a homeowner will receive a loan modification, win in court, stop every sale, eliminate a valid mortgage debt, or keep a home regardless of the facts.

What an experienced lawyer can do is protect the homeowner's rights, identify available defenses, hold the lender to its legal obligations, explain options clearly, and advocate for the best possible outcome under the circumstances.

Be cautious of anyone who promises a guaranteed modification or claims they can stop foreclosure without reviewing the court file, loan history, and financial situation. In New York foreclosure defense, details matter.

Documents to Gather Before Speaking With a Lawyer

You do not need to have everything perfectly organized before asking for help. But if possible, gather the following documents before your consultation:

- Foreclosure summons and complaint

- 90-day notice or other letters from the lender

- Mortgage, note, and any loan modification agreements

- Recent mortgage statements

- Payment history or proof of payments

- Court orders, motions, or notices of sale

- Loan modification applications and denial letters

- Household income information

- Tax bills, insurance documents, and escrow statements

- Any bankruptcy, debt collection, or judgment paperwork

If you cannot find some documents, do not let that stop you from calling. A lawyer may be able to obtain court filings or help identify what is missing.

Frequently Asked Questions

Can foreclosure defense lawyers stop foreclosure in New York? They may be able to stop, delay, or challenge foreclosure depending on the facts. Options may include legal defenses, settlement conferences, loan modification, bankruptcy, emergency motions, appeals, or negotiated resolutions. No outcome can be guaranteed.

When should I contact a foreclosure lawyer? As early as possible. The best time is when you fall behind, receive a 90-day notice, or are served with a summons and complaint. If a sale is already scheduled, you should seek advice immediately because late-stage options are more limited.

What if I already applied for a loan modification? You may still benefit from legal help. A lawyer can review whether the application was handled properly, whether documents were incorrectly rejected, whether the denial makes sense, and whether other options are available.

Do I have to leave my home as soon as foreclosure starts? No. In New York, foreclosure is a court process. A homeowner generally does not have to leave simply because a lawsuit was filed. Even after a foreclosure sale, there may be additional legal steps before an eviction can occur.

Can bankruptcy help me keep my home? It can in some cases. Chapter 13 may allow certain homeowners to catch up on mortgage arrears over time while stopping foreclosure activity through the automatic stay. Whether bankruptcy makes sense depends on income, expenses, equity, arrears, and other debts.

What if the lender waited years to restart the foreclosure case? Statute of limitations issues may be important in New York foreclosure cases, especially after changes under the Foreclosure Abuse Prevention Act. These issues are complex and should be reviewed by counsel. CGW has discussed the New York Foreclosure Abuse Prevention Act in more detail.

Speak With a New York Foreclosure Defense Lawyer Before Deadlines Pass

Foreclosure is stressful, but you do not have to navigate it alone. Whether you just received a notice, have been served with a lawsuit, are in settlement conferences, or are facing a scheduled auction, getting legal guidance early may preserve more options.

Clair Gjertsen & Weathers PLLC helps homeowners in Westchester County, Rockland County, Putnam County, Orange County, Dutchess County, Bronx County, and the Lower Hudson Valley evaluate foreclosure defense, loan modification, bankruptcy, loss mitigation, appeals, short sales, and related strategies.

If your home is at risk, contact Clair Gjertsen & Weathers PLLC to discuss your situation with a qualified New York attorney. This article provides general information and is not a substitute for legal advice about your specific case.

Debt Lawsuits vs. Foreclosure in New York: Key Differences

Falling behind on a mortgage or other bills can be overwhelming. When legal papers start to arrive, many people feel anxious and unsure where to turn, especially when their home and basic stability seem at risk.

In New York, different kinds of creditors use different legal tools. Mortgage lenders start foreclosure cases, while credit card companies, medical providers, and other lenders usually file debt lawsuits. Knowing which one you are dealing with affects your options, your timeline, and the impact on your home and income. The goal of this article is to explain these processes in clear terms so you can start to regain a sense of control and make thoughtful decisions.

Every situation is unique, and nothing here is a substitute for legal advice. But understanding the basics can help you pause, get oriented, and take the next step with more confidence.

What a Foreclosure Case Means for Your Home in New York

Foreclosure is the court process a mortgage lender uses to try to sell your home after a default on the loan. In New York, foreclosures are usually handled in Supreme Court, and the lender must file a lawsuit to begin.

Some key features of New York foreclosure cases include:

- The process starts with a summons and complaint delivered to you

- The case is judicial, which means a judge is involved in each stage

- For many owner-occupied homes, the court holds settlement conferences

- Timelines can be longer than in many other states

Those settlement conferences are designed to help homeowners and lenders talk about options. Depending on the facts, that might include a loan modification, repayment plan, short sale, or another resolution. These conferences are not just formalities; they can be meaningful chances to work out an agreement.

In foreclosure, what is at stake is your ownership of the property itself. That does not mean you lose the home right away, or at all, but the risk is real if the case goes forward and the court eventually allows a sale.

There is another piece many people are not aware of: a possible deficiency judgment. If the home is sold and the sale price is less than what is owed on the mortgage, the lender may ask the court for a money judgment for the difference. That unpaid balance can then be collected like other debts and may lead to additional collection efforts down the road.

Defenses and options in foreclosure cases are very fact-specific. For example, timing, past payment history, prior modifications, and how the lender handled notices can all matter. Speaking with a lawyer who handles foreclosure and bankruptcy work in New York early in the process often keeps more choices open.